Page 190 - ELT_1_1st April 2020_Vol 372_Part

P. 190

76 EXCISE LAW TIMES [ Vol. 372

amended by clause 60 of the Finance Bill, 2010, Notification No. 91/2010-Cus.,

dated 6-9-2010, the Court had granted limited relief to the extent that it had set

aside the proviso to Notification No. 25/2010-Cus., dated 27-2-2010, which pro-

vided that the notification exempting goods falling under Tariff Item 2716 00 00

from the whole of the duty of Customs leviable thereon which is specified in the

First Schedule to the Customs Tariff Act, 1975 would not apply to electrical ener-

gy falling under Tariff Item 2716 00 00 removed from SEZ to DTA or non-

processing areas of SEZs.

12. It may be noted that the above notification stood rescinded by a no-

tification dated 10th May, 2010 except as respects things done or omitted to be

done before such rescission. Thus, the life of the said notification was only for a

short period of less than three months.

13. Insofar as the other notifications which were subject matter of chal-

lenge in that petition are concerned, it appears that the Division Bench did not

deem it fit to grant the reliefs prayed for in the petition and restricted the same to

the above Notification No. 25/2010-Cus., dated 27-2-2010 and also held that the

petitioners are entitled to exemption from payment of Customs duty for the pe-

riod 26-6-2009 to 15-9-2010 on the electricity cleared to DTA, that is, for the peri-

od during from which the Notification No. 25/2010-Cus., dated 27-2-2010 which

amended Notification No. 21/2002-Cus., dated 1-3-2002 was given retrospective

effect till Notification No. 21/2002-Cus. came to be further amended vide Notifi-

cation No. 91/2010-Cus., dated 6-9-2010.

14. It may be noted that vide Notification No. 12/2012-Cus., dated 17-

3-2012, Notification No. 21/2002-Cus., dated 1-3-2002 came to be superseded.

However, the said notification and the subsequent notification amending the

said notification, viz., Notification No. 26/2012-Cus., dated 18-4-2012 were not

challenged by the petitioners, though the writ petition was pending before the

Court at the relevant time.

15. It may be noted that not only did the Division Bench, after pro-

pounding the principles on which reliance has been placed on behalf of the peti-

tioners to seek declaratory relief, not granted the relief as prayed for in the earlier

writ petition and restricted it to the period from 26-6-2009 to 15-9-2010, after the

judgment was delivered, the petitioners upon noticing the same, moved a Note

for Speaking to the Minutes, praying for the relief in the following terms :

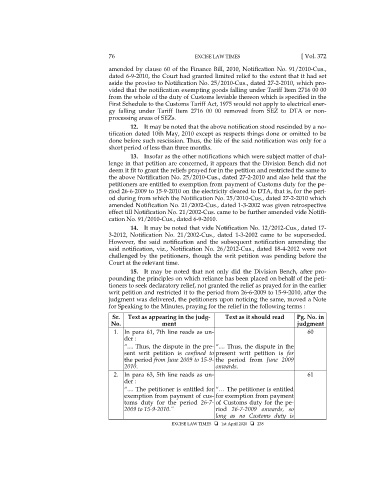

Sr. Text as appearing in the judg- Text as it should read Pg. No. in

No. ment judgment

1. In para 61, 7th line reads as un- 60

der :

“.... Thus, the dispute in the pre- “.... Thus, the dispute in the

sent writ petition is confined to present writ petition is for

the period from June 2009 to 15-9- the period from June 2009

2010. onwards.

2. In para 63, 5th line reads as un- 61

der :

“.... The petitioner is entitled for “… The petitioner is entitled

exemption from payment of cus- for exemption from payment

toms duty for the period 26-7- of Customs duty for the pe-

2009 to 15-9-2010.” riod 26-7-2009 onwards, so

long as no Customs duty is

EXCISE LAW TIMES 1st April 2020 238