Page 265 - ELT_1_1st April 2020_Vol 372_Part

P. 265

2020 ] KAIPAN PAN MASALA PVT. LTD. v. COMMR. OF CGST, EX. AND CUS., BHOPAL 151

which was denied by Adjudicating Authority. This denial of re-test which is a

vested right and required to be permitted as per is evident from the instruction

of C.B.E. & C. Thus, there was non-observance of principle of natural justice, and

therefore, the impugned order is liable to be set aside on this ground alone.

14. Ld. AR on behalf of Revenue supports the impugned order on the

ground contained therein and argued that appellants kept on changing classifica-

tion between CT and ZST depending upon the duty structure favourable to them

under the compounded levy from time to time, although the product manufac-

tured remained the same. When the notifications issued under compounded levy

scheme prescribed lower duty on CT, the appellant described the product as CT

but when duty on ZST was less, the classification was changed as ZST with in-

tention to pay lower rate of duty.

15. We have considered the case records and submissions made by the

parties.

16. As stated earlier the issue involved in this case is regarding classifi-

cation of the products manufactured by the appellants. It is the contention of the

Revenue that the appellant has manufactured the ZST which attracted the higher

rate of duty under the compounded levy scheme than the CT at the relevant pe-

riod, and therefore, the appellant has misdeclared the goods and paid less central

excise duty under the compounded levy scheme. On the other hand the appel-

lant’s contention is that they have manufactured only CT during the relevant

period for which appropriate declaration has been filed with the Department as

per the requirement under compounded levy scheme. For better appreciation of

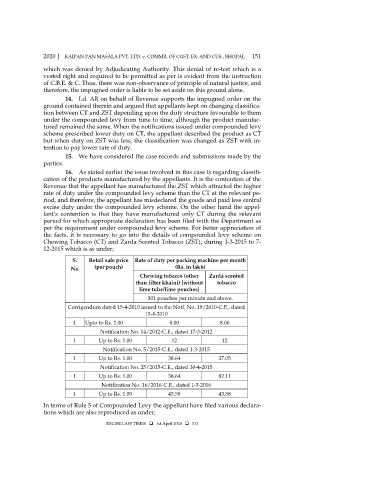

the facts, it is necessary to go into the details of compounded levy scheme on

Chewing Tobacco (CT) and Zarda Scented Tobacco (ZST), during 1-3-2015 to 7-

12-2015 which is as under;

S. Retail sale price Rate of duty per packing machine per month

No (per pouch) (Rs. in lakh)

Chewing tobacco (other Zarda scented

than filter khaini) [without tobacco

lime tube/lime pouches]

301 pouches per minute and above.

Corrigendum dated 15-4-2010 issued to the Notf. No. 19/2010-C.E., dated

13-4-2010

1 Upto to Rs. 1.00 8.00 8.00

Notification No. 14/2012-C.E., dated 17-3-2012

1 Up to Rs. 1.00 12 12

Notification No. 5/2015-C.E., dated 1-3-2015

1 Up to Rs. 1.00 38.64 27.05

Notification No. 25/2015-C.E., dated 30-4-2015

1 Up to Rs. 1.00 38.64 82.11

Notification No. 16/2016-C.E., dated 1-3-2016

1 Up to Rs. 1.00 43.58 43.58

In terms of Rule 5 of Compounded Levy the appellant have filed various declara-

tions which are also reproduced as under;

EXCISE LAW TIMES 1st April 2020 313