Page 145 - GSTL_26th March 2020_Vol 34_Part 4

P. 145

2020 ] IN RE : VILAS CHANDANMAL GANDHI 655

the Sh. B.C. Khandale, Asstt. Commissioner of S.T. Pune-2, appeared and made

oral submissions.

5. Observations :

5.1 We have gone through the facts of the case, documents on record

and submissions made by both, the applicant as well as the jurisdictional officer.

The basic issue before us is, whether GST is leviable on sale of TDR/FSI received

as consideration for surrendering the joint rights in land in terms of Develop-

ment Control Regulations.

5.2 We find that vide F. No. 354/32/2019-TRU, dated the 14th May,

2019, the Government of India, Ministry of Finance, Department of Revenue (Tax

Research Unit), New Delhi has issued FAQs (Part II) on real estate. Sr. No. 7 of

the same is reproduced below :-

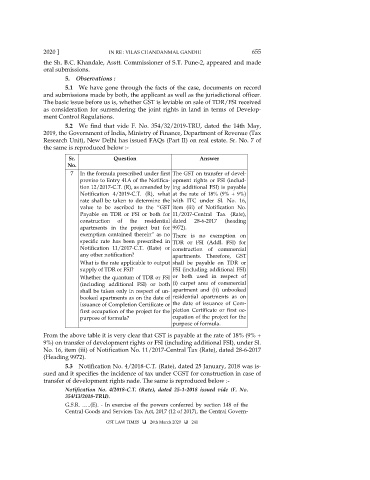

Sr. Question Answer

No.

7 In the formula prescribed under first The GST on transfer of devel-

proviso to Entry 41A of the Notifica- opment rights or FSI (includ-

tion 12/2017-C.T. (R), as amended by ing additional FSI) is payable

Notification 4/2019-C.T. (R), what at the rate of 18% (9% + 9%)

rate shall be taken to determine the with ITC under Sl. No. 16,

value to be ascribed to the “GST item (iii) of Notification No.

Payable on TDR or FSI or both for 11/2017-Central Tax (Rate),

construction of the residential dated 28-6-2017 (heading

apartments in the project but for 9972).

exemption contained therein” as no There is no exemption on

specific rate has been prescribed in TDR or FSI (Addl. FSI) for

Notification 11/2017-C.T. (Rate) or construction of commercial

any other notification? apartments. Therefore, GST

What is the rate applicable to output shall be payable on TDR or

supply of TDR or FSI? FSI (including additional FSI)

Whether the quantum of TDR or FSI or both used in respect of

(including additional FSI) or both (i) carpet area of commercial

shall be taken only in respect of un- apartment and (ii) unbooked

booked apartments as on the date of residential apartments as on

issuance of Completion Certificate or the date of issuance of Com-

first occupation of the project for the pletion Certificate or first oc-

purpose of formula? cupation of the project for the

purpose of formula.

From the above table it is very clear that GST is payable at the rate of 18% (9% +

9%) on transfer of development rights or FSI (including additional FSI), under Sl.

No. 16, item (iii) of Notification No. 11/2017-Central Tax (Rate), dated 28-6-2017

(Heading 9972).

5.3 Notification No. 4/2018-C.T. (Rate), dated 25 January, 2018 was is-

sued and it specifies the incidence of tax under CGST for construction in case of

transfer of development rights nade. The same is reproduced below :-

Notification No. 4/2018-C.T. (Rate), dated 25-1-2018 issued vide (F. No.

354/13/2018-TRU).

G.S.R. …..(E). - In exercise of the powers conferred by section 148 of the

Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Govern-

GST LAW TIMES 26th March 2020 241