Page 182 - GSTL_2nd April 2020_Vol 35_Part 1

P. 182

84 GST LAW TIMES [ Vol. 35

GOKUL AGRO RESOURCES LTD.

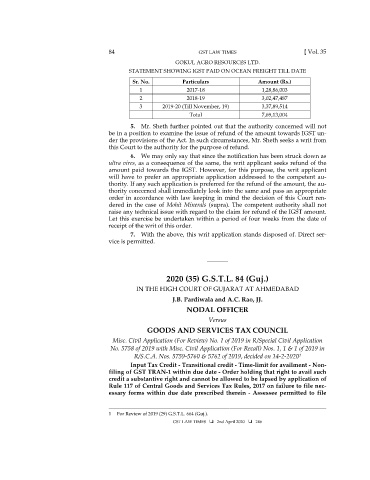

STATEMENT SHOWING IGST PAID ON OCEAN FREIGHT TILL DATE

Sr. No. Particulars Amount (Rs.)

1 2017-18 1,28,86,003

2 2018-19 3,02,47,487

3 2019-20 (Till November, 19) 3,37,89,514

Total 7,69,13,004

5. Mr. Sheth further pointed out that the authority concerned will not

be in a position to examine the issue of refund of the amount towards IGST un-

der the provisions of the Act. In such circumstances, Mr. Sheth seeks a writ from

this Court to the authority for the purpose of refund.

6. We may only say that since the notification has been struck down as

ultra vires, as a consequence of the same, the writ applicant seeks refund of the

amount paid towards the IGST. However, for this purpose, the writ applicant

will have to prefer an appropriate application addressed to the competent au-

thority. If any such application is preferred for the refund of the amount, the au-

thority concerned shall immediately look into the same and pass an appropriate

order in accordance with law keeping in mind the decision of this Court ren-

dered in the case of Mohit Minerals (supra). The competent authority shall not

raise any technical issue with regard to the claim for refund of the IGST amount.

Let this exercise be undertaken within a period of four weeks from the date of

receipt of the writ of this order.

7. With the above, this writ application stands disposed of. Direct ser-

vice is permitted.

_______

2020 (35) G.S.T.L. 84 (Guj.)

IN THE HIGH COURT OF GUJARAT AT AHMEDABAD

J.B. Pardiwala and A.C. Rao, JJ.

NODAL OFFICER

Versus

GOODS AND SERVICES TAX COUNCIL

Misc. Civil Application (For Review) No. 1 of 2019 in R/Special Civil Application

No. 5758 of 2019 with Misc. Civil Application (For Recall) Nos. 1, 1 & 1 of 2019 in

R/S.C.A. Nos. 5759-5760 & 5762 of 2019, decided on 14-2-2020

1

Input Tax Credit - Transitional credit - Time-limit for availment - Non-

filing of GST TRAN-1 within due date - Order holding that right to avail such

credit a substantive right and cannot be allowed to be lapsed by application of

Rule 117 of Central Goods and Services Tax Rules, 2017 on failure to file nec-

essary forms within due date prescribed therein - Assessee permitted to file

________________________________________________________________________

1 For Review of 2019 (29) G.S.T.L. 664 (Guj.).

GST LAW TIMES 2nd April 2020 246