Page 28 - GSTL_23rd April 2020_Vol 35_Part 4

P. 28

J56 GST LAW TIMES [ Vol. 35

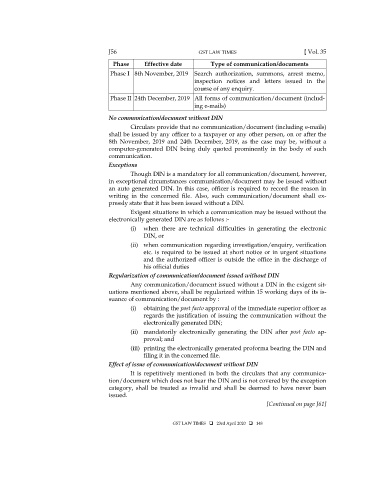

Phase Effective date Type of communication/documents

Phase I 8th November, 2019 Search authorization, summons, arrest memo,

inspection notices and letters issued in the

course of any enquiry.

Phase II 24th December, 2019 All forms of communication/document (includ-

ing e-mails)

No communication/document without DIN

Circulars provide that no communication/document (including e-mails)

shall be issued by any officer to a taxpayer or any other person, on or after the

8th November, 2019 and 24th December, 2019, as the case may be, without a

computer-generated DIN being duly quoted prominently in the body of such

communication.

Exceptions

Though DIN is a mandatory for all communication/document, however,

in exceptional circumstances communication/document may be issued without

an auto generated DIN. In this case, officer is required to record the reason in

writing in the concerned file. Also, such communication/document shall ex-

pressly state that it has been issued without a DIN.

Exigent situations in which a communication may be issued without the

electronically generated DIN are as follows :-

(i) when there are technical difficulties in generating the electronic

DIN, or

(ii) when communication regarding investigation/enquiry, verification

etc. is required to be issued at short notice or in urgent situations

and the authorized officer is outside the office in the discharge of

his official duties

Regularization of communication/document issued without DIN

Any communication/document issued without a DIN in the exigent sit-

uations mentioned above, shall be regularized within 15 working days of its is-

suance of communication/document by :

(i) obtaining the post facto approval of the immediate superior officer as

regards the justification of issuing the communication without the

electronically generated DIN;

(ii) mandatorily electronically generating the DIN after post facto ap-

proval; and

(iii) printing the electronically generated proforma bearing the DIN and

filing it in the concerned file.

Effect of issue of communication/document without DIN

It is repetitively mentioned in both the circulars that any communica-

tion/document which does not bear the DIN and is not covered by the exception

category, shall be treated as invalid and shall be deemed to have never been

issued.

[Continued on page J61]

GST LAW TIMES 23rd April 2020 148