Page 126 - GSTL_30th April 2020_Vol 35_Part 5

P. 126

612 GST LAW TIMES [ Vol. 35

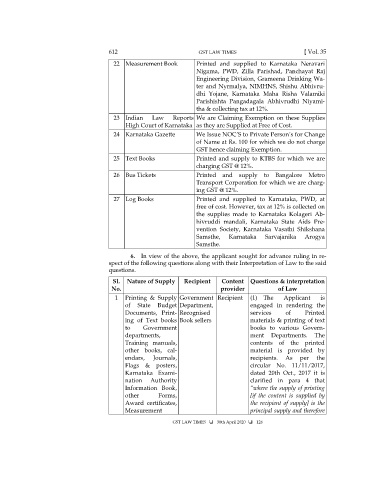

22 Measurement Book Printed and supplied to Karnataka Neravari

Nigama, PWD, Zilla Parishad, Panchayat Raj

Engineering Division, Grameena Drinking Wa-

ter and Nyrmalya, NIMHNS, Shishu Abhivru-

dhi Yojane, Karnataka Maha Risha Valamiki

Parishishta Pangadagala Abhivrudhi Niyami-

tha & collecting tax at 12%.

23 Indian Law Reports We are Claiming Exemption on these Supplies

High Court of Karnataka as they are Supplied at Free of Cost.

24 Karnataka Gazette We Issue NOC’S to Private Person’s for Change

of Name at Rs. 100 for which we do not charge

GST hence claiming Exemption.

25 Text Books Printed and supply to KTBS for which we are

charging GST @ 12%.

26 Bus Tickets Printed and supply to Bangalore Metro

Transport Corporation for which we are charg-

ing GST @ 12%.

27 Log Books Printed and supplied to Karnataka, PWD, at

free of cost. However, tax at 12% is collected on

the supplies made to Karnataka Kolageri Ab-

hivruddi mandali, Karnataka State Aids Pre-

vention Society, Karnataka Vasathi Shikshana

Samsthe, Karnataka Sarvajanika Arogya

Samsthe.

6. In view of the above, the applicant sought for advance ruling in re-

spect of the following questions along with their Interpretation of Law to the said

questions.

Sl. Nature of Supply Recipient Content Questions & interpretation

No. provider of Law

1 Printing & Supply Government Recipient (1) The Applicant is

of State Budget Department, engaged in rendering the

Documents, Print- Recognised services of Printed

ing of Text books Book sellers materials & printing of text

to Government books to various Govern-

departments, ment Departments. The

Training manuals, contents of the printed

other books, cal- material is provided by

endars, Journals, recipients. As per the

Flags & posters, circular No. 11/11/2017,

Karnataka Exami- dated 20th Oct., 2017 it is

nation Authority clarified in para 4 that

Information Book, “where the supply of printing

other Forms, [if the content is supplied by

Award certificates, the recipient of supply] is the

Measurement principal supply and therefore

GST LAW TIMES 30th April 2020 126