Page 133 - GSTL_30th April 2020_Vol 35_Part 5

P. 133

2020 ] IN RE : DEPARTMENT OF PRINTING, STATIONERY AND PUBLICATIONS 619

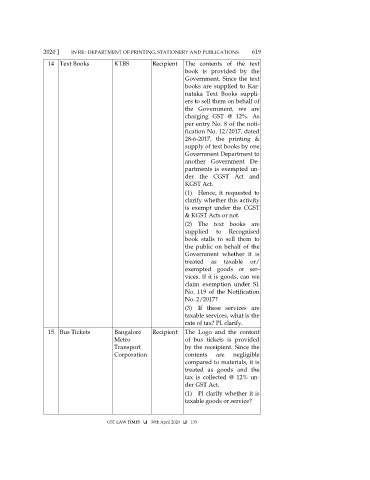

14 Text Books KTBS Recipient The contents of the text

book is provided by the

Government. Since the text

books are supplied to Kar-

nataka Text Books suppli-

ers to sell them on behalf of

the Government, we are

charging GST @ 12%. As

per entry No. 8 of the noti-

fication No. 12/2017, dated

28-6-2017, the printing &

supply of text books by one

Government Department to

another Government De-

partments is exempted un-

der the CGST Act and

KGST Act.

(1) Hence, it requested to

clarify whether this activity

is exempt under the CGST

& KGST Acts or not.

(2) The text books are

supplied to Recognised

book stalls to sell them to

the public on behalf of the

Government whether it is

treated as taxable or/

exempted goods or ser-

vices. If it is goods, can we

claim exemption under Sl.

No. 119 of the Notification

No. 2/2017?

(3) If these services are

taxable services, what is the

rate of tax? Pl. clarify.

15 Bus Tickets Bangalore Recipient The Logo and the content

Metro of bus tickets is provided

Transport by the receipient. Since the

Corporation contents are negligible

compared to materials, it is

treated as goods and the

tax is collected @ 12% un-

der GST Act.

(1) Pl clarify whether it is

taxable goods or service?

GST LAW TIMES 30th April 2020 133