Page 106 - GSTL_7th May 2020_Vol 36_Part 1

P. 106

64 GST LAW TIMES [ Vol. 36

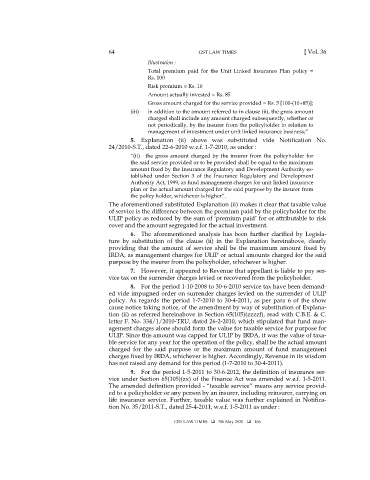

Illustration :

Total premium paid for the Unit Linked Insurance Plan policy =

Rs. 100

Risk premium = Rs. 10

Amount actually invested = Rs. 85

Gross amount charged for the service provided = Rs. 5 [100-(10+85)];

(iii) in addition to the amount referred to in clause (ii), the gross amount

charged shall include any amount charged subsequently, whether or

not periodically, by the insurer from the policyholder in relation to

management of investment under unit linked insurance business;”

5. Explanation (ii) above was substituted vide Notification No.

24/2010-S.T., dated 22-6-2010 w.e.f. 1-7-2010, as under :

“(ii) the gross amount charged by the insurer from the policyholder for

the said service provided or to be provided shall be equal to the maximum

amount fixed by the Insurance Regulatory and Development Authority es-

tablished under Section 3 of the Insurance Regulatory and Development

Authority Act, 1999, as fund management charges for unit linked insurance

plan or the actual amount charged for the said purpose by the insurer from

the policy holder, whichever is higher”.

The aforementioned substituted Explanation (ii) makes it clear that taxable value

of service is the difference between the premium paid by the policyholder for the

ULIP policy as reduced by the sum of ‘premium paid’ for or attributable to risk

cover and the amount segregated for the actual investment.

6. The aforementioned analysis has been further clarified by Legisla-

ture by substitution of the clause (ii) in the Explanation hereinabove, clearly

providing that the amount of service shall be the maximum amount fixed by

IRDA, as management charges for ULIP or actual amounts charged for the said

purpose by the insurer from the policyholder, whichever is higher.

7. However, it appeared to Revenue that appellant is liable to pay ser-

vice tax on the surrender charges levied or recovered from the policyholder.

8. For the period 1-10-2008 to 30-6-2010 service tax have been demand-

ed vide impugned order on surrender charges levied on the surrender of ULIP

policy. As regards the period 1-7-2010 to 30-4-2011, as per para 6 of the show

cause notice taking notice, of the amendment by way of substitution of Explana-

tion (ii) as referred hereinabove in Section 65(105)(zzzzf), read with C.B.E. & C.

letter F. No. 334/1/2010-TRU, dated 26-2-2010, which stipulated that fund man-

agement charges alone should form the value for taxable service for purpose for

ULIP. Since this amount was capped for ULIP by IRDA, it was the value of taxa-

ble service for any year for the operation of the policy, shall be the actual amount

charged for the said purpose or the maximum amount of fund management

charges fixed by IRDA, whichever is higher. Accordingly, Revenue in its wisdom

has not raised any demand for this period (1-7-2010 to 30-4-2011).

9. For the period 1-5-2011 to 30-6-2012, the definition of insurance ser-

vice under Section 65(105)(zx) of the Finance Act was amended w.e.f. 1-5-2011.

The amended definition provided - “taxable service” means any service provid-

ed to a policyholder or any person by an insurer, including reinsurer, carrying on

life insurance service. Further, taxable value was further explained in Notifica-

tion No. 35/2011-S.T., dated 25-4-2011, w.e.f. 1-5-2011 as under :

GST LAW TIMES 7th May 2020 106