Page 172 - GSTL_7th May 2020_Vol 36_Part 1

P. 172

130 GST LAW TIMES [ Vol. 36

tone of colour, transparency (or opaqueness), and must, on application in

thin layers by brush or otherwise, dry within a short period by evaporation

of its volatile solvents (alcohol, ether, benzine, spirits or turpentine etc.)

leaving a film of smooth lustrous (sometimes purposely dull,), elastic oil

and resin, impervious to its surrounding atmospheric conditions”

Therefore varnish, as is commonly understood, is a colourless liquid applied

over substances to lend it a particular effect (whether glossy or matte) and for

protective purposes.

3.3.3 Their product, (they mentioned in invoice as technical varnish,

medium or tinting ink) on the other hand is not used for protecting any article of

substance, rather it is used for printing of substance by applying a process which

is called printing. As it is used for printing of substance by applying a process

which can be called printing, so it should not be treated anything other than

printing ink.

4. The Central Goods & Services Tax and Customs Commissionerate,

Vadodara-II, has submitted the point-wise compliance report/comments, as

under :

(i) The activity is manufacturing of “varnish”, “Medium” and

“Printing ink” are “ongoing activity” and not a proposed one; (these de-

tails are on the basis of manufacturing product shown in their Excise Re-

turns).

(ii) This is a fresh application in GST and with reference to Central

Excise, M/s. Flint Group is already quoting Chapter Heading against

“Varnishes and Medium”.

(iii) From the Excise returns filed by M/s. Flint Group, it is ob-

served that during the Central Excise regime, “Medium” a manufactur-

ing item classified under Chapter S/Heading 3208 90 11 attracts duty @

12.5%, “Printing ink” which is classified under Chapter S/Heading 3215

11 90 attracts duty @ 12.5%, “varnish” is classified under 3209 10 10 and

attracts duty @ 12.5%; Thus, though all the three items are classified un-

der different Chapter Heading, they attract uniform rate of duty;

(iv) In GST Regime, M/s. Flint Group, in GSTR-3B, as per GST

REG-26 - “details of goods supplied by the business”, the following are

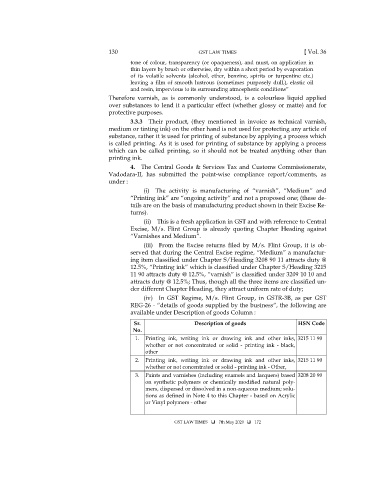

available under Description of goods Column :

Sr. Description of goods HSN Code

No.

1. Printing ink, writing ink or drawing ink and other inks, 3215 11 90

whether or not concentrated or solid - printing ink - black,

other

2. Printing ink, writing ink or drawing ink and other inks, 3215 11 90

whether or not concentrated or solid - printing ink - Other,

3. Paints and varnishes (including enamels and lacquers) based 3208 20 90

on synthetic polymers or chemically modified natural poly-

mers, dispersed or dissolved in a non-aqueous medium; solu-

tions as defined in Note 4 to this Chapter - based on Acrylic

or Vinyl polymers - other

GST LAW TIMES 7th May 2020 172