Page 34 - GSTL_7th May 2020_Vol 36_Part 1

P. 34

J16 GST LAW TIMES [ Vol. 36

Ruling :

The Advance Ruling on question posed before the Authority is answered as

under :

(I) Whether amount recovered from the employees towards pa-

rental insurance premium payable to the insurance company

would be deemed as “Supply of Service” by the applicant to

its employees?

Ans. : Answered in negative.

(II) If the first question is answered in affirmative, whether the

value of aforesaid supply would be NIL, being provided in

the capacity of a “Pure Agent”? If valuation is not accepted as

NIL, what would be the value of such supply?

Ans. : As the answer of question No. I is in negative this ques-

tion doesn’t need answer.

(III) If GST is payable on the such amount recovered from the em-

ployees, whether the proportionate GST paid by the applicant

to insurance company towards parental insurance would be

admissible as input tax credit against supply of insurance ser-

vices for employees’ parents?

Ans. : Answered in negative.

Conclusion

Thus, the recovery of parents’ health insurance premium amount from

employee, subsequent deposit with insurance company cannot be treated as

supply of service in terms of Section 7 of CGST Act, 2017 and non-taxable under

GST law.

_______

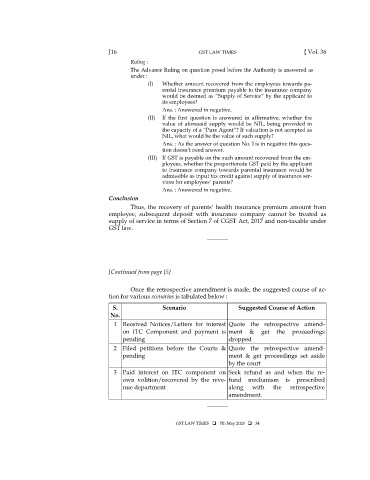

[Continued from page J5]

Once the retrospective amendment is made, the suggested course of ac-

tion for various scenarios is tabulated below :

S. Scenario Suggested Course of Action

No.

1 Received Notices/Letters for interest Quote the retrospective amend-

on ITC Component and payment is ment & get the proceedings

pending dropped

2 Filed petitions before the Courts & Quote the retrospective amend-

pending ment & get proceedings set aside

by the court

3 Paid interest on ITC component on Seek refund as and when the re-

own volition/recovered by the reve- fund mechanism is prescribed

nue department along with the retrospective

amendment.

_______

GST LAW TIMES 7th May 2020 34