Page 172 - GSTL_14th May 2020_Vol 36_Part 2

P. 172

274 GST LAW TIMES [ Vol. 36

above, we find that the construction services provided by the applicant are not in

the nature of composite supply and, therefore, the tax liability thereof has to be

determined by treating the same different from the supply of transmission and

distribution of electricity.

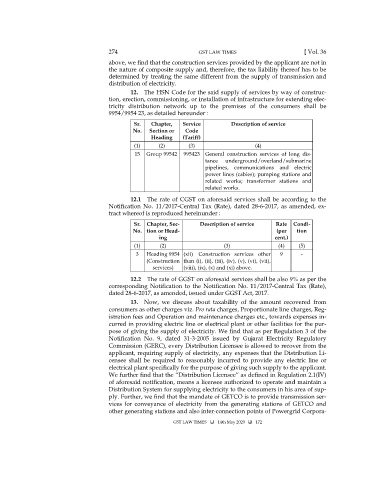

12. The HSN Code for the said supply of services by way of construc-

tion, erection, commissioning, or installation of infrastructure for extending elec-

tricity distribution network up to the premises of the consumers shall be

9954/9954 23, as detailed hereunder :

Sr. Chapter, Service Description of service

No. Section or Code

Heading (Tariff)

(1) (2) (3) (4)

15 Group 99542 995423 General construction services of long dis-

tance underground/overland/submarine

pipelines, communications and electric

power lines (cables); pumping stations and

related works; transformer stations and

related works.

12.1 The rate of CGST on aforesaid services shall be according to the

Notification No. 11/2017-Central Tax (Rate), dated 28-6-2017, as amended, ex-

tract whereof is reproduced hereinunder :

Sr. Chapter, Sec- Description of service Rate Condi-

No. tion or Head- (per tion

ing cent.)

(1) (2) (3) (4) (5)

3 Heading 9954 (xii) Construction services other 9 -

(Construction than (i), (ii), (iii), (iv), (v), (vi), (vii),

services) (viii), (ix), (x) and (xi) above.

12.2 The rate of GGST on aforesaid services shall be also 9% as per the

corresponding Notification to the Notification No. 11/2017-Central Tax (Rate),

dated 28-6-2017, as amended, issued under GGST Act, 2017.

13. Now, we discuss about taxability of the amount recovered from

consumers as other charges viz. Pro rata charges, Proportionate line charges, Reg-

istration fees and Operation and maintenance charges etc., towards expenses in-

curred in providing electric line or electrical plant or other facilities for the pur-

pose of giving the supply of electricity. We find that as per Regulation 3 of the

Notification No. 9, dated 31-3-2005 issued by Gujarat Electricity Regulatory

Commission (GERC), every Distribution Licensee is allowed to recover from the

applicant, requiring supply of electricity, any expenses that the Distribution Li-

censee shall be required to reasonably incurred to provide any electric line or

electrical plant specifically for the purpose of giving such supply to the applicant.

We further find that the “Distribution Licensee” as defined in Regulation 2.1(IV)

of aforesaid notification, means a licensee authorized to operate and maintain a

Distribution System for supplying electricity to the consumers in his area of sup-

ply. Further, we find that the mandate of GETCO is to provide transmission ser-

vices for conveyance of electricity from the generating stations of GETCO and

other generating stations and also inter-connection points of Powergrid Corpora-

GST LAW TIMES 14th May 2020 172