Page 125 - GSTL_11th June 2020_Vol 37_Part 2

P. 125

2020 ] GATEWAY HOTELS v. COMMISSIONER OF CUSTOMS, C. EX. & S.T., COCHIN 211

Restaurant service - Whether ‘exempted service’ during the period

from 1-7-2012 to 31-3-2013 - No abatement availed in respect of restaurant ser-

vice - As per Rule 2C of Service Tax (Determination of Value) Rules, 2006, val-

ue of service portion involved in supply of food or any other article of human

consumption or any drink in a restaurant being fixed as 40% of the total value

on the condition that Cenvat credit on inputs not taken, the remaining portion

of the value would neither be considered as an abatement nor as an exemption

and accordingly restaurant service would not be covered under the definition

of input service and provisions of Rule 6 of Cenvat Credit Rules, 2004 not ap-

plicable. [para 6]

Demand - Limitation - Extended period - Appellants although availed

the total Cenvat credit of ` 23 lakhs (approx.) whereas vide the impugned or-

der, Commissioner demanding more than ` 80 lakhs which is more than the

total credit availed - Further, for the period April, 2008 to March, 2012, entire

demand is barred by limitation, show cause notice being issued on 21-10-2013

for the period April, 2008 to March, 2012 which is beyond the limitation period

of one year - Also, Extended period not invocable, law on the point when not

clear and definition of exempted service changed from time to time and inter-

pretational issue involved - Substantial demand for the period from April,

2008 to March, 2012 entirely time-barred - Rules 6 and 14 of Cenvat Credit

Rules, 2004. [para 6]

Appeals allowed

CASES CITED

Aster Pvt. Ltd. v. Commissioner — 2016 (43) S.T.R. 411 (Tribunal) — Referred............................ [Para 4.3]

Cranes & Structural Engineers v. Commissioner

— 2017 (347) E.L.T. 112 (Tribunal) — Referred ......................................................................... [Para 4.3]

Final Order No. 21118/2018, dated 8-8-2018 by CESTAT, Bangalore — Referred .................. [Paras 4.2, 6]

Kerala Classified Hotels and Resorts Association v. Union of India

— 2013 (31) S.T.R. 257 (Ker.) — Relied on ............................................................................ [Paras 4.2, 6]

State of HP v. Associated Hotels of India Ltd. — 2017 (50) S.T.R. 80 (S.C.)

= 2015 (330) E.L.T. 3 (S.C.) — Referred ...................................................................................... [Para 4.2]

Union of India v. Kerala Bar Hotels Association — 2014 (36) S.T.R. 1205 (Ker.) — Referred ...... [Para 4.2]

REPRESENTED BY : Shri Jose Jacob, Advocate, for the Appellant.

Shri V. Veerabhadra Reddy, AR, for the Respondent.

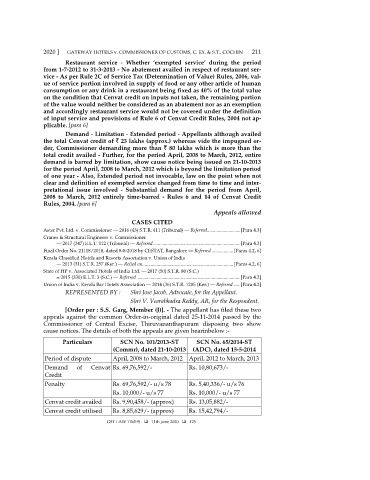

[Order per : S.S. Garg, Member (J)]. - The appellant has filed these two

appeals against the common Order-in-original dated 25-11-2014 passed by the

Commissioner of Central Excise, Thiruvananthapuram disposing two show

cause notices. The details of both the appeals are given hearinbelow :-

Particulars SCN No. 101/2013-ST SCN No. 65/2014-ST

(Commr), dated 21-10-2013 (ADC), dated 15-5-2014

Period of dispute April, 2008 to March, 2012 April, 2012 to March, 2013

Demand of Cenvat Rs. 69,76,592/- Rs. 10,80,673/-

Credit

Penalty Rs. 69,76,592/- u/s 78 Rs. 5,40,336/- u/s 76

Rs. 10,000/- u/s 77 Rs. 10,000/- u/s 77

Cenvat credit availed Rs. 9,90,458/- (approx) Rs. 13,05,882/-

Cenvat credit utilised Rs. 8,85,629/- (approx) Rs. 15,42,794/-

GST LAW TIMES 11th June 2020 125