Page 186 - GSTL_11th June 2020_Vol 37_Part 2

P. 186

272 GST LAW TIMES [ Vol. 37

Provided further that the unique number generated under sub-rule (1) shall

be valid for a period of fifteen days for updation of Part B of FORM GST

EWB-01.

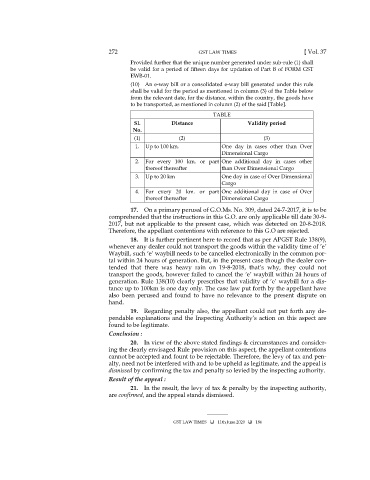

(10) An e-way bill or a consolidated e-way bill generated under this rule

shall be valid for the period as mentioned in column (3) of the Table below

from the relevant date, for the distance, within the country, the goods have

to be transported, as mentioned in column (2) of the said [Table].

TABLE

Sl. Distance Validity period

No.

(1) (2) (3)

1. Up to 100 km. One day in cases other than Over

Dimensional Cargo

2. For every 100 km. or part One additional day in cases other

thereof thereafter than Over Dimensional Cargo

3. Up to 20 km One day in case of Over Dimensional

Cargo

4. For every 20 km. or part One additional day in case of Over

thereof thereafter Dimensional Cargo

17. On a primary perusal of G.O.Ms. No. 309, dated 24-7-2017, it is to be

comprehended that the instructions in this G.O. are only applicable till date 30-9-

2017, but not applicable to the present case, which was detected on 20-8-2018.

Therefore, the appellant contentions with reference to this G.O are rejected.

18. It is further pertinent here to record that as per APGST Rule 138(9),

whenever any dealer could not transport the goods within the validity time of ’e’

Waybill, such ‘e’ waybill needs to be cancelled electronically in the common por-

tal within 24 hours of generation. But, in the present case though the dealer con-

tended that there was heavy rain on 19-8-2018, that’s why, they could not

transport the goods, however failed to cancel the ‘e’ waybill within 24 hours of

generation. Rule 138(10) clearly prescribes that validity of ‘e’ waybill for a dis-

tance up to 100km is one day only. The case law put forth by the appellant have

also been perused and found to have no relevance to the present dispute on

hand.

19. Regarding penalty also, the appellant could not put forth any de-

pendable explanations and the Inspecting Authority’s action on this aspect are

found to be legitimate.

Conclusion :

20. In view of the above stated findings & circumstances and consider-

ing the clearly envisaged Rule provision on this aspect, the appellant contentions

cannot be accepted and fount to be rejectable. Therefore, the levy of tax and pen-

alty, need not be interfered with and to be upheld as legitimate, and the appeal is

dismissed by confirming the tax and penalty so levied by the inspecting authority.

Result of the appeal :

21. In the result, the levy of tax & penalty by the inspecting authority,

are confirmed, and the appeal stands dismissed.

_______

GST LAW TIMES 11th June 2020 186