Page 94 - GSTL_18th June 2020_Vol 37_Part 3

P. 94

308 GST LAW TIMES [ Vol. 37

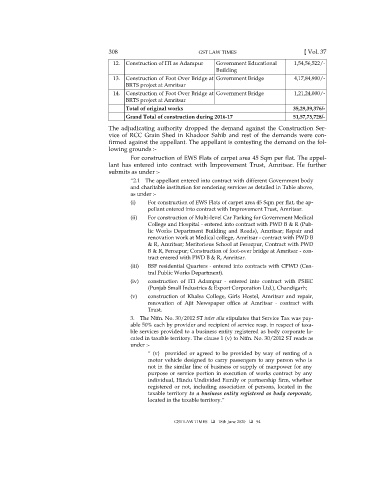

12. Construction of ITI as Adampur Government Educational 1,54,56,522/-

Building

13. Construction of Foot Over Bridge at Government Bridge 4,17,84,900/-

BRTS project at Amritsar

14. Construction of Foot Over Bridge at Government Bridge 1,21,24,000/-

BRTS project at Amritsar

Total of original works 35,29,39,376/-

Grand Total of construction during 2016-17 51,57,75,728/-

The adjudicating authority dropped the demand against the Construction Ser-

vice of RCC Grain Shed in Khadoor Sahib and rest of the demands were con-

firmed against the appellant. The appellant is contesting the demand on the fol-

lowing grounds :-

For construction of EWS Flats of carpet area 45 Sqm per flat. The appel-

lant has entered into contract with Improvement Trust, Amritsar. He further

submits as under :-

“2.1 The appellant entered into contract with different Government body

and charitable institution for rendering services as detailed in Table above,

as under :-

(i) For construction of EWS Flats of carpet area 45 Sqm per flat, the ap-

pellant entered into contract with Improvement Trust, Amritsar.

(ii) For construction of Multi-level Car Parking for Government Medical

College and Hospital - entered into contract with PWD B & R (Pub-

lic Works Department Building and Roads), Amritsar; Repair and

renovation work at Medical college, Amritsar - contract with PWD B

& R, Amritsar; Meritorious School at Ferozpur, Contract with PWD

B & R, Ferozpur; Construction of foot-over bridge at Amritsar - con-

tract entered with PWD B & R, Amritsar.

(iii) BSF residential Quarters - entered into contracts with CPWD (Cen-

tral Public Works Department).

(iv) construction of ITI Adampur - entered into contract with PSIEC

(Punjab Small Industries & Export Corporation Ltd.), Chandigarh;

(v) construction of Khalsa College, Girls Hostel, Amritsar and repair,

renovation of Ajit Newspaper office at Amritsar - contract with

Trust.

3. The Ntfn. No. 30/2012 ST inter alia stipulates that Service Tax was pay-

able 50% each by provider and recipient of service resp. in respect of taxa-

ble services provided to a business entity registered as body corporate lo-

cated in taxable territory. The clause 1 (v) to Ntfn. No. 30/2012 ST reads as

under :-

“ (v) provided or agreed to be provided by way of renting of a

motor vehicle designed to carry passengers to any person who is

not in the similar line of business or supply of manpower for any

purpose or service portion in execution of works contract by any

individual, Hindu Undivided Family or partnership firm, whether

registered or not, including association of persons, located in the

taxable territory to a business entity registered as body corporate,

located in the taxable territory.”

GST LAW TIMES 18th June 2020 94