Page 33 - GSTL_16th July 2020_Vol. 38_Part 3

P. 33

2020 ] A POSSIBLE REMEDY TO AMENDMENT OF RULE 96(10) J75

(d) Merchant exporters procuring the goods at concessional rate of 0.1%

vide Notification No. 40/2017-C.T. (R), dated 23-10-2017 and Notifi-

cation No. 41/2017-IGST (R), dated 23-10-2017.

Not being aware of the aforesaid restrictions, certain exporters availed the benefit

of above-mentioned notifications and simultaneously claimed refund under 2nd

option. This was questioned by the department and they demanded the payback of

the refunds/exemptions availed by them.

In many of the above mentioned cases, paying back the amount of ex-

emption would be advantageous due to various reasons. For example, the ex-

porters would have availed the IGST exemption of ` 1,00,000/- at the time of

procurements and has paid IGST and claimed refund of 2,50,000/- at the time of

exports. In this scenario, the paying back of exemption would be preferable to

losing the option of encasing the refund on output. However, it would not be so

if both IGST & BCD have to be repaid. In view of the authors, mere foregoing

IGST exemption would entitle the refund under 2nd option to the exporters but

it is possible the department officers may not accept this view and raise dispute

in appellate fora.

Recently, the Government vide Notification No. 16/2020-C.T., dated

23-3-2020 has made an amendment by inserting following explanation to Rule

96(10) of CGST Rules, 2017 as amended (with retrospective effect from

23-10-2017).

“Explanation. - For the purpose of this sub-rule, the benefit of the notifications

mentioned therein shall not be considered to have been availed only where

the registered person has paid Integrated Goods and Services Tax and Com-

pensation Cess on inputs and has availed exemption of only Basic Customs

Duty (BCD) under the said notifications.”

By virtue of the above amendment, the option of claiming refund under 2nd op-

tion is not restricted in case exporters avail only BCD exemption but pay IGST on

the raw materials. Since the amendment was made retrospectively it seems possi-

ble for exporters to repay IGST along with interest and claim refund under 2nd

option. They will be able to claim ITC of IGST so paid.

The aforesaid restriction was challenged before HC’s [Granuels India Lim-

ited (WP No. 24021/2019) before the High Court of Andhra Pradesh and Zaveri &

Co. (P.) Ltd. v. Union of India - SCA No. 15091 of 2018 before the High Court of

Gujarat] and is pending for final decision as on date. In this background, the

suggested course of action is tabulated below :

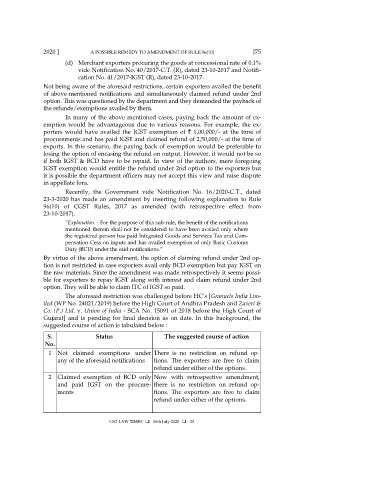

S. Status The suggested course of action

No.

1 Not claimed exemptions under There is no restriction on refund op-

any of the aforesaid notifications tions. The exporters are free to claim

refund under either of the options.

2 Claimed exemption of BCD only Now with retrospective amendment,

and paid IGST on the procure- there is no restriction on refund op-

ments tions. The exporters are free to claim

refund under either of the options.

GST LAW TIMES 16th July 2020 33