Page 105 - GSTL_23rd July 2020_Vol 38_Part 4

P. 105

2020 ] IN RE : NAVBHARAT LPG BOTTLING COMPANY 471

wherein in Sr. No. 165, in column (3), the words, “to household domestic consumers

or”, was omitted and a new Serial Number 165A was inserted after Sr. No. 165 in

Schedule-I of the said notification as under :

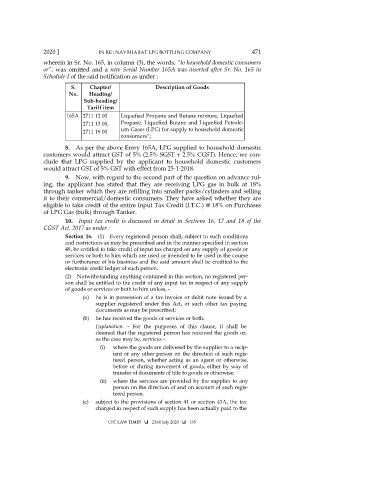

S. Chapter/ Description of Goods

No. Heading/

Sub-heading/

Tariff item

165A 2711 12 00 Liquefied Propane and Butane mixture, Liquefied

2711 13 00, Propane, Liquefied Butane and Liquefied Petrole-

2711 19 00 um Gases (LPG) for supply to household domestic

consumers”;

8. As per the above Entry 165A, LPG supplied to household domestic

customers would attract GST of 5% (2.5% SGST + 2.5% CGST). Hence, we con-

clude that LPG supplied by the applicant to household domestic customers

would attract GST of 5% GST with effect from 25-1-2018.

9. Now, with regard to the second part of the question on advance rul-

ing, the applicant has stated that they are receiving LPG gas in bulk at 18%

through tanker which they are refilling into smaller packs/cylinders and selling

it to their commercial/domestic consumers. They have asked whether they are

eligible to take credit of the entire Input Tax Credit (I.T.C.) @ 18% on Purchases

of LPG Gas (bulk) through Tanker.

10. Input tax credit is discussed in detail in Sections 16, 17 and 18 of the

CGST Act, 2017 as under :

Section 16. (1) Every registered person shall, subject to such conditions

and restrictions as may be prescribed and in the manner specified in section

49, be entitled to take credit of input tax charged on any supply of goods or

services or both to him which are used or intended to be used in the course

or furtherance of his business and the said amount shall be credited to the

electronic credit ledger of such person.

(2) Notwithstanding anything contained in this section, no registered per-

son shall be entitled to the credit of any input tax in respect of any supply

of goods or services or both to him unless, -

(a) he is in possession of a tax invoice or debit note issued by a

supplier registered under this Act, or such other tax paying

documents as may be prescribed;

(b) he has received the goods or services or both.

Explanation. - For the purposes of this clause, it shall be

deemed that the registered person has received the goods or,

as the case may be, services -

(i) where the goods are delivered by the supplier to a recip-

ient or any other person on the direction of such regis-

tered person, whether acting as an agent or otherwise,

before or during movement of goods, either by way of

transfer of documents of title to goods or otherwise;

(ii) where the services are provided by the supplier to any

person on the direction of and on account of such regis-

tered person.

(c) subject to the provisions of section 41 or section 43A, the tax

charged in respect of such supply has been actually paid to the

GST LAW TIMES 23rd July 2020 105