Page 39 - GSTL_23rd July 2020_Vol 38_Part 4

P. 39

2020 ] DECODING SECTION 73 OF CGST ACT, 2017 J97

73 may be served up to 5th November, 2022. Similarly, for FY 2018-19 where due

date of annual return has been fixed at 30th September, 2020, notice under Sec-

tion 73 may be served up to 30th June, 2023. It is pertinent to note that actual date

of filing of annual return has no relevance as far as service of notice under Sec-

tion 73 is concerned.

Is it mandatory for the proper officer to take cognizance of the submission made

by the person?

Where a submission is made by the person against notice served by

proper officer, it is mandatory for the officer to take the cognizance of the same.

Section 73(9) binds the officer to consider the representation made by the person.

It is upon the officer to either accept or reject the representation. Where the of-

ficer proceeds with proceedings under Section 73 after rejecting the representa-

tion, he must place on record the reasons in writing while issuing order u/s.

73(10). Where the officer fails to provide suitable reply against the representa-

tion, the order under Section 73 is liable to be quashed.

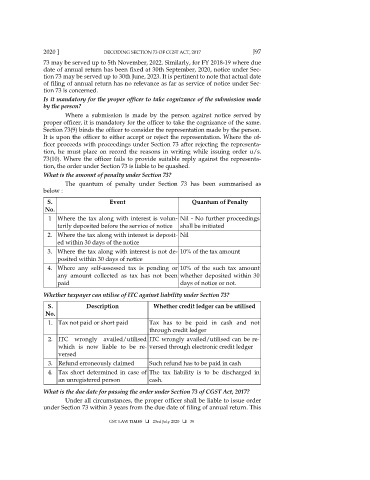

What is the amount of penalty under Section 73?

The quantum of penalty under Section 73 has been summarised as

below :

S. Event Quantum of Penalty

No.

1 Where the tax along with interest is volun- Nil - No further proceedings

tarily deposited before the service of notice shall be initiated

2. Where the tax along with interest is deposit- Nil

ed within 30 days of the notice

3. Where the tax along with interest is not de- 10% of the tax amount

posited within 30 days of notice

4. Where any self-assessed tax is pending or 10% of the such tax amount

any amount collected as tax has not been whether deposited within 30

paid days of notice or not.

Whether taxpayer can utilise of ITC against liability under Section 73?

S. Description Whether credit ledger can be utilised

No.

1. Tax not paid or short paid Tax has to be paid in cash and not

through credit ledger

2. ITC wrongly availed/utilised ITC wrongly availed/utilised can be re-

which is now liable to be re- versed through electronic credit ledger

versed

3. Refund erroneously claimed Such refund has to be paid in cash

4. Tax short determined in case of The tax liability is to be discharged in

an unregistered person cash.

What is the due date for passing the order under Section 73 of CGST Act, 2017?

Under all circumstances, the proper officer shall be liable to issue order

under Section 73 within 3 years from the due date of filing of annual return. This

GST LAW TIMES 23rd July 2020 39