Page 49 - GSTL_23rd July 2020_Vol 38_Part 4

P. 49

2020 ] QUESTION-ANSWER BOX J107

There is nothing in your query to show as to on what basis the Department is

seeking to challenge your classification. We presume that they are contesting

with Heading 3402 of Customs Tariff Act, 1975 in mind.

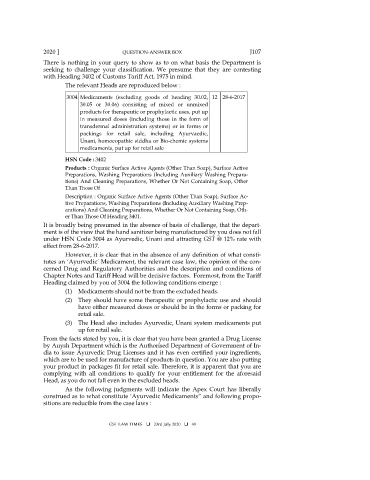

The relevant Heads are reproduced below :

3004 Medicaments (excluding goods of heading 30.02, 12 28-6-2017

30.05 or 30.06) consisting of mixed or unmixed

products for therapeutic or prophylactic uses, put up

in measured doses (including those in the form of

transdermal administration systems) or in forms or

packings for retail sale, including Ayurvaedic,

Unani, homoeopathic siddha or Bio-chemic systems

medicaments, put up for retail sale

HSN Code : 3402

Products : Organic Surface Active Agents (Other Than Soap), Surface Active

Preparations, Washing Preparations (Including Auxiliary Washing Prepara-

tions) And Cleaning Preparations, Whether Or Not Containing Soap, Other

Than Those Of

Description : Organic Surface Active Agents (Other Than Soap), Surface Ac-

tive Preparations, Washing Preparations (Including Auxiliary Washing Prep-

arations) And Cleaning Preparations, Whether Or Not Containing Soap, Oth-

er Than Those Of Heading 3401.

It is broadly being presumed in the absence of basis of challenge, that the depart-

ment is of the view that the hand sanitizer being manufactured by you does not fall

under HSN Code 3004 as Ayurvedic, Unani and attracting GST @ 12% rate with

effect from 28-6-2017.

However, it is clear that in the absence of any definition of what consti-

tutes an ‘Ayurvedic’ Medicament, the relevant case law, the opinion of the con-

cerned Drug and Regulatory Authorities and the description and conditions of

Chapter Notes and Tariff Head will be decisive factors. Foremost, from the Tariff

Heading claimed by you of 3004 the following conditions emerge :

(1) Medicaments should not be from the excluded heads.

(2) They should have some therapeutic or prophylactic use and should

have either measured doses or should be in the forms or packing for

retail sale.

(3) The Head also includes Ayurvedic, Unani system medicaments put

up for retail sale.

From the facts stated by you, it is clear that you have been granted a Drug License

by Auysh Department which is the Authorised Department of Government of In-

dia to issue Ayurvedic Drug Licenses and it has even certified your ingredients,

which are to be used for manufacture of products in question. You are also putting

your product in packages fit for retail sale. Therefore, it is apparent that you are

complying with all conditions to qualify for your entitlement for the aforesaid

Head, as you do not fall even in the excluded heads.

As the following judgments will indicate the Apex Court has liberally

construed as to what constitute ‘Ayurvedic Medicaments” and following propo-

sitions are reducible from the case laws :

GST LAW TIMES 23rd July 2020 49