Page 150 - GSTL_6th August 2020_Vol 39_Part 1

P. 150

76 GST LAW TIMES [ Vol. 39

(a) The person should provide services in relation to transportation of

goods;

(b) The goods should be transported through road;

(c) Consignment note is to be issued.

The Notification offers two options for discharging GST to a person qualifying as

a GTA under the explanation laid out under Entry No. 9(iii) :

(i) Pay tax at 5% which shall be paid under reverse charge mechanism

by the recipient (ITC of the tax charged on inputs used by the GTA

shall not be available to the GTA);

(ii) Pay tax at 12% under forward charge mechanism (GTA is eligible to

avail ITC on the inputs used in the course/furtherance of business).

2.12 Applicant has opted for the second option (ii above) and has sub-

mitted that it has contract with the end customer and hence its services would be

classified under Service Code 9965 11. On delivery of goods POSCO-MAH

acknowledges completion of the transportation services by stamping the con-

signment note issued by the Applicant.

2.13 Even in cases, where the third-party transporter has charged the

GST @ 12% after issuing consignment note (wherein Applicant is named as the

consignor and the consignee is the customer to whose factory the goods are de-

livered), the Applicant would be eligible to avail the input tax credit as it is

charging GST @ 12% on its outward supply of GTA services.

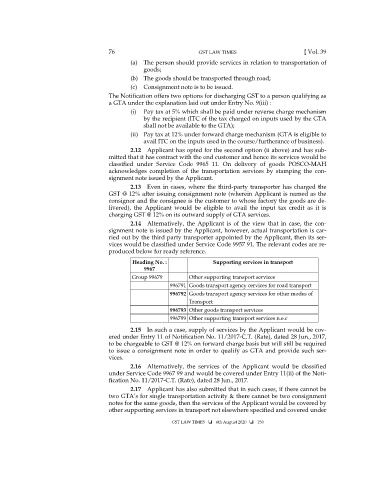

2.14 Alternatively, the Applicant is of the view that in case, the con-

signment note is issued by the Applicant, however, actual transportation is car-

ried out by the third party transporter appointed by the Applicant, then its ser-

vices would be classified under Service Code 9957 91. The relevant codes are re-

produced below for ready reference.

Heading No. : Supporting services in transport

9967

Group 99679 Other supporting transport services

996791 Goods transport agency cervices for road transport

996792 Goods transport agency services for other modes of

Transport

996793 Other goods transport services

996799 Other supporting transport services n.e.c

2.15 In such a case, supply of services by the Applicant would be cov-

ered under Entry 11 of Notification No. 11/2017-C.T. (Rate), dated 28 Jun., 2017,

to be chargeable to GST @ 12% on forward charge basis but will still be required

to issue a consignment note in order to qualify as GTA and provide such ser-

vices.

2.16 Alternatively, the services of the Applicant would be classified

under Service Code 9967 99 and would be covered under Entry 11(ii) of the Noti-

fication No. 11/2017-C.T. (Rate), dated 28 Jun., 2017.

2.17 Applicant has also submitted that in such cases, if there cannot be

two GTA’s for single transportation activity & there cannot be two consignment

notes for the same goods, then the services of the Applicant would be covered by

other supporting services in transport not elsewhere specified and covered under

GST LAW TIMES 6th August 2020 150