Page 127 - GSTL_13th August 2020_Vol 39_Part 2

P. 127

2020 ] IN RE : APSARA CO-OPERATIVE HOUSING SOCIETY LTD. 213

the applicant for the benefit of its members will come under the scope of busi-

ness.

5.11 In view of the above we are of the opinion that all the conditions

stipulated for considering the activities of applicant as “Supply” under the GST

Law have been fulfilled.

5.12 Applicant has contended that the Applicant Society and its mem-

bers cannot be treated as distinct persons, by citing the “principle of mutuality”.

We have already found above that both, the Applicant as well as its members are

to be considered as separate person. The contention made by the Applicant with

regard to the principle of mutuality to establish their claim that the Applicant

Society and its member are not distinct entity is not tenable in so far as taxability

in the GST regime is concerned.

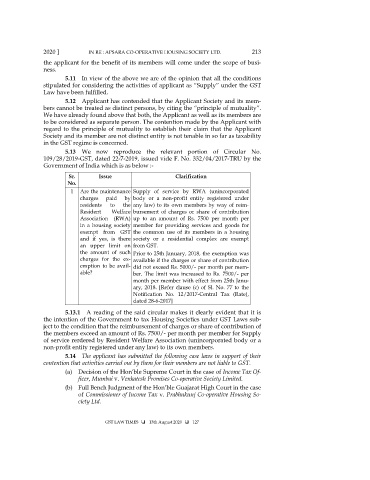

5.13 We now reproduce the relevant portion of Circular No.

109/28/2019-GST, dated 22-7-2019, issued vide F. No. 332/04/2017-TRU by the

Government of India which is as below :-

Sr. Issue Clarification

No.

1 Are the maintenance Supply of service by RWA (unincorporated

charges paid by body or a non-profit entity registered under

residents to the any law) to its own members by way of reim-

Resident Welfare bursement of charges or share of contribution

Association (RWA) up to an amount of Rs. 7500 per month per

in a housing society member for providing services and goods for

exempt from GST the common use of its members in a housing

and if yes, is there society or a residential complex are exempt

an upper limit on from GST.

the amount of such Prior to 25th January, 2018, the exemption was

charges for the ex- available if the charges or share of contribution

emption to be avail- did not exceed Rs. 5000/- per month per mem-

able? ber. The limit was increased to Rs. 7500/- per

month per member with effect from 25th Janu-

ary, 2018. [Refer clause (c) of Sl. No. 77 to the

Notification No. 12/2017-Central Tax (Rate),

dated 28-6-2017]

5.13.1 A reading of the said circular makes it clearly evident that it is

the intention of the Government to tax Housing Societies under GST Laws sub-

ject to the condition that the reimbursement of charges or share of contribution of

the members exceed an amount of Rs. 7500/- per month per member for Supply

of service rerdered by Resident Welfare Association (unincorporated body or a

non-profit entity registered under any law) to its own members.

5.14 The applicant has submitted the following case laws in support of their

contention that activities carried out by them for their members are not liable to GST.

(a) Decision of the Hon’ble Supreme Court in the case of Income Tax Of-

ficer, Mumbai v. Venkatesh Promises Co-operative Society Limited.

(b) Full Bench Judgment of the Hon’ble Guajarat High Court in the case

of Commissioner of Income Tax v. Prabhukunj Co-operative Housing So-

ciety Ltd.

GST LAW TIMES 13th August 2020 127