Page 32 - GSTL_13th August 2020_Vol 39_Part 2

P. 32

J40 GST LAW TIMES [ Vol. 39

HSN Code 4401 for classification of ‘wood in logs’ on the basis of earlier VAT

classification and discharged tax liability as per tariff rate under GST.

Accordingly, the traders supplied ‘wood in logs’ under HSN/Chapter

Heading 4401 to the various paper industries and charged GST @ 5% against Sl.

No. 198 in terms of Notification No. 1/2017-C.T. (Rate), dated 28-6-2017 and as

per rate specified in the Schedule-I to the said Notification.

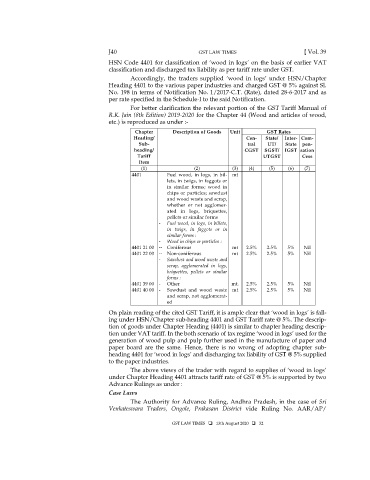

For better clarification the relevant portion of the GST Tariff Manual of

R.K. Jain (8th Edition) 2019-2020 for the Chapter 44 (Wood and articles of wood,

etc.) is reproduced as under :-

Chapter Description of Goods Unit GST Rates

Heading/ Cen- State/ Inter- Com-

Sub- tral UT/ State pen-

heading/ CGST SGST/ IGST sation

Tariff UTGST Cess

Item

(1) (2) (3) (4) (5) (6) (7)

4401 Fuel wood, in logs, in bil- mt

lets, in twigs, in faggots or

in similar forms; wood in

chips or particles; sawdust

and wood waste and scrap,

whether or not agglomer-

ated in logs, briquettes,

pellets or similar forms

- Fuel wood, in logs, in billets,

in twigs, in faggots or in

similar forms :

- Wood in chips or particles :

4401 21 00 -- Coniferous mt 2.5% 2.5% 5% Nil

4401 22 00 -- Non-coniferous mt 2.5% 2.5% 5% Nil

- Sawdust and wood waste and

scrap, agglomerated in logs,

briquettes, pellets or similar

forms :

4401 39 00 - Other mt. 2.5% 2.5% 5% Nil

4401 40 00 - Sawdust and wood waste mt 2.5% 2.5% 5% Nil

and scrap, not agglomerat-

ed

On plain reading of the cited GST Tariff, it is ample clear that ‘wood in logs’ is fall-

ing under HSN/Chapter sub-heading 4401 and GST Tariff rate @ 5%. The descrip-

tion of goods under Chapter Heading (4401) is similar to chapter heading descrip-

tion under VAT tariff. In the both scenario of tax regime ‘wood in logs’ used for the

generation of wood pulp and pulp further used in the manufacture of paper and

paper board are the same. Hence, there is no wrong of adopting chapter sub-

heading 4401 for ‘wood in logs’ and discharging tax liability of GST @ 5% supplied

to the paper industries.

The above views of the trader with regard to supplies of ‘wood in logs’

under Chapter Heading 4401 attracts tariff rate of GST @ 5% is supported by two

Advance Rulings as under :

Case Laws

The Authority for Advance Ruling, Andhra Pradesh, in the case of Sri

Venkateswara Traders, Ongole, Prakasam District vide Ruling No. AAR/AP/

GST LAW TIMES 13th August 2020 32