Page 90 - GSTL_13th August 2020_Vol 39_Part 2

P. 90

176 GST LAW TIMES [ Vol. 39

(b) Purchase of the tobacco leaves from other dealers and sell them to

the clients within India and overseas.

(c) Threshing and redrying of the tobacco leaves in their threshing

premises and selling them to the clients in India and to export to

various countries.

(d) Engaging in threshing of redrying of tobacco leaves on job work ba-

sis for other traders or manufacturers.

We have gone through the facts of the case as submitted by the applicant with

respect to the relevant legal position. As seen from the above it is felt that the

transactions of tobacco from auction platform to the supply made to the exporter

are to be interpreted in the light of the relevant notifications and to decide the

rate of tax accordingly. As seen from the different stages of commodity i.e., from

the leaves stage to the final product (manufactured tobacco), the green leaf

plucked from the plant undergoes different types of curing to reduce the level of

moisture to the maximum extent for sustainability and to continue as leaf for fur-

ther process. The tobacco leaf will be entitled as a commercial commodity only

drying (Curing) and normally put to trade in form of bundles. The same will be

traded between the farmer and the trader and trader to trader/manufacturer and

so on. As envisaged from the entries under GST, there are four different entries

for tobacco, one under Schedule-I. Liable @ 5% (CGST 2.5% and SGST 2.5%) and

the remaining heads are in Schedule-IV liable 28% (CGST-14% and SGST 14%).

And there is an entry of tobacco leaves under Reverse charge mechanism also as

explained below :

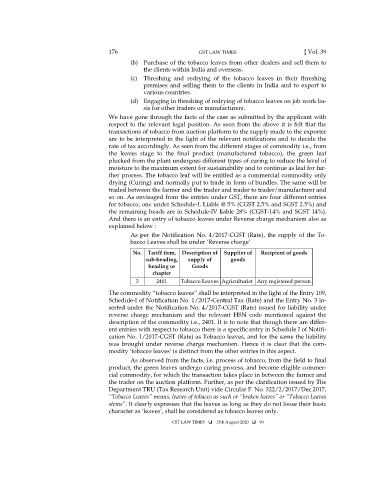

As per the Notification No. 4/2017-CGST (Rate), the supply of the To-

bacco Leaves shall be under ‘Reverse charge’

No. Tariff item, Description of Supplier of Recipient of goods

sub-heading, supply of goods

heading or Goods

chapter

3 2401 Tobacco Leaves Agriculturist Any registered person

The commodity “tobacco leaves” shall be interpreted in the light of the Entry 109,

Schedule-I of Notification No. 1/2017-Central Tax (Rate) and the Entry No. 3 in-

serted under the Notification No. 4/2017-CGST (Rate) issued for liability under

reverse charge mechanism and the relevant HSN code mentioned against the

description of the commodity i.e., 2401. It is to note that though there are differ-

ent entries with respect to tobacco there is a specific entry in Schedule I of Notifi-

cation No. 1/2017-CGST (Rate) as Tobacco leaves, and for the same the liability

was brought under reverse charge mechanism. Hence it is clear that the com-

modity ‘tobacco leaves’ is distinct from the other entries in this aspect.

As observed from the facts, i.e. process of tobacco, from the field to final

product, the green leaves undergo curing process, and become eligible commer-

cial commodity, for which the transaction takes place in between the farmer and

the trader on the auction platform. Further, as per the clarification issued by The

Department TRU (Tax Research Unit) vide Circular F. No. 322/2/2017/Dec.2017,

“Tobacco Leaves” means, leaves of tobacco as such or “broken leaves” or “Tobacco Leaves

stems”. It clearly expresses that the leaves as long as they do not loose their basic

character as ‘leaves’, shall be considered as tobacco leaves only.

GST LAW TIMES 13th August 2020 90