Page 163 - GSTL_20th August 2020_Vol 39_Part 3

P. 163

2020 ] IN RE : OCEAN SPARKLE LIMITED 377

terms of S. No. 17(vii) of the Notification No. 1/2018-I.T. (Rate), dated 25-1-2018

(as amended), which covers “Time charter of vessels for transport of goods.”

Before proceeding with the submission on merits, it would be pertinent

to refer to the competing entries under which the services rendered by the Tug

Jupiter, let out on charter basis by the Applicant to RIL, could be classified,

which are set out as below vide Notification No. 1/2018-I.T. (Rate), dated 25-1-

2018 read with Notification No. 8/2017-I.T. (Rate), dated 28-6-2017.

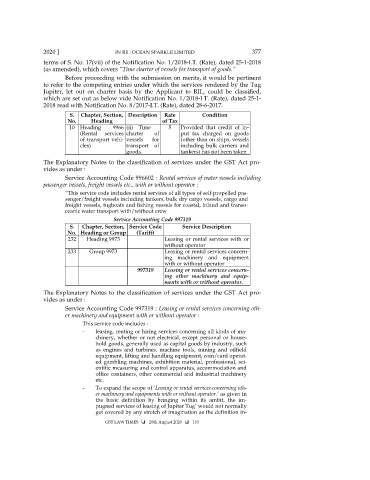

S. Chapter, Section, Description Rate Condition

No. Heading of Tax

10 Heading 9966 (ii) Time 5 Provided that credit of in-

(Rental services charter of put tax charged on goods

of transport vehi- vessels for (other than on ships, vessels

cles) transport of including bulk carriers and

goods. tankers) has not been taken

The Explanatory Notes to the classification of services under the GST Act pro-

vides as under :

Service Accounting Code 996602 : Rental services of water vessels including

passenger vessels, freight vessels etc., with or without operator :

“This service code includes rental services of all types of self-propelled pas-

senger/freight vessels including tankers, bulk dry cargo vessels, cargo and

freight vessels, tugboats and fishing vessels for coastal, inland and transo-

ceanic water transport with/without crew

Service Accounting Code 997319

S. Chapter, Section, Service Code Service Description

No. Heading or Group (Tariff)

232 Heading 9973 Leasing or rental services with or

without operator

233 Group 9973 Leasing or rental services concern-

ing machinery and equipment

with or without operator

997319 Leasing or rental services concern-

ing other machinery and equip-

ments with or without operator.

The Explanatory Notes to the classification of services under the GST Act pro-

vides as under :

Service Accounting Code 997319 : Leasing or rental services concerning oth-

er machinery and equipment with or without operator :

This service code includes :

- leasing, renting or hiring services concerning all kinds of ma-

chinery, whether or not electrical, except personal or house-

hold goods, generally used as capital goods by industry, such

as engines and turbines, machine tools, mining and oilfield

equipment, lifting and handling equipment, coin/card operat-

ed gambling machines, exhibition material, professional, sci-

entific measuring and control apparatus, accommodation and

office containers, other commercial and industrial machinery

etc.

- To expand the scope of ‘Leasing or rental services concerning oth-

er machinery and equipments with or without operator.’ as given in

the basic definition by bringing within its ambit, the im-

pugned services of leasing of Jupiter Tug’ would not normally

get covered by any stretch of imagination as the definition in-

GST LAW TIMES 20th August 2020 163