Page 77 - GSTL_20th August 2020_Vol 39_Part 3

P. 77

2020 ] IN RE : LAKSHMI TULASI QUALITY FUELS 291

5. Applicant’s interpretation of law and facts :

The applicant’s contention is that she is eligible for the exemption from

payment of GST granted under Sl. No. 13 of Exemption Notification, i.e. Notifica-

tion No. 9/2017, dated 28-6-2017, the reference of which is extracted below :

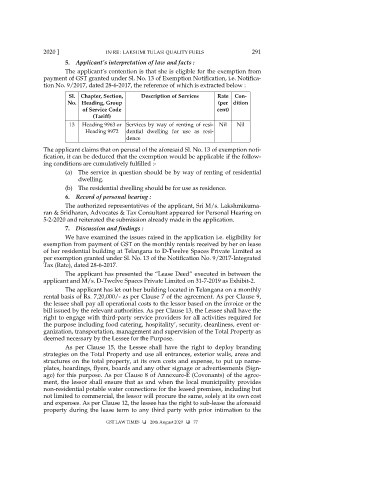

Sl. Chapter, Section, Description of Services Rate Con-

No. Heading, Group (per dition

of Service Code cent)

(Tariff)

13 Heading 9963 or Services by way of renting of resi- Nil Nil

Heading 9972 dential dwelling for use as resi-

dence

The applicant claims that on perusal of the aforesaid Sl. No. 13 of exemption noti-

fication, it can be deduced that the exemption would be applicable if the follow-

ing conditions are cumulatively fulfilled :-

(a) The service in question should be by way of renting of residential

dwelling.

(b) The residential dwelling should be for use as residence.

6. Record of personal hearing :

The authorized representatives of the applicant, Sri M/s. Lakshmikuma-

ran & Sridharan, Advocates & Tax Consultant appeared for Personal Hearing on

5-2-2020 and reiterated the submission already made in the application.

7. Discussion and findings :

We have examined the issues raised in the application i.e. eligibility for

exemption from payment of GST on the monthly rentals received by her on lease

of her residential building at Telangana to D-Twelve Spaces Private Limited as

per exemption granted under Sl. No. 13 of the Notification No. 9/2017-Integrated

Tax (Rate), dated 28-6-2017.

The applicant has presented the “Lease Deed” executed in between the

applicant and M/s. D-Twelve Spaces Private Limited on 31-7-2019 as Exhibit-2.

The applicant has let out her building located in Telangana on a monthly

rental basis of Rs. 7,20,000/- as per Clause 7 of the agreement. As per Clause 9,

the lessee shall pay all operational costs to the lessor based on the invoice or the

bill issued by the relevant authorities. As per Clause 13, the Lessee shall have the

right to engage with third-party service providers for all activities required for

the purpose including food catering, hospitality’, security, cleanliness, event or-

ganization, transportation, management and supervision of the Total Property as

deemed necessary by the Lessee for the Purpose.

As per Clause 15, the Lessee shall have the right to deploy branding

strategies on the Total Property and use all entrances, exterior walls, areas and

structures on the total property, at its own costs and expense, to put up name-

plates, hoardings, flyers, boards and any other signage or advertisements (Sign-

age) for this purpose. As per Clause 8 of Annexure-E (Covenants) of the agree-

ment, the lessor shall ensure that as and when the local municipality provides

non-residential potable water connections for the leased premises, including but

not limited to commercial, the lessor will procure the same, solely at its own cost

and expenses. As per Clause 12, the lessee has the right to sub-lease the aforesaid

property during the lease term to any third party with prior intimation to the

GST LAW TIMES 20th August 2020 77