Page 107 - GSTL_27th August 2020_Vol 39_Part 4

P. 107

2020 ] IN RE : ATAL BIHARI VAJPAYEE INSTITUTE OF GOOD GOVERNANCE 433

ment/local Authority in response to views called by the Authority of advance

ruling on the application submitted by the Applicant.

6. Record of personal hearing :

Shri Navneet Garg, CA & Shri Girish Trivedi, Chief Manager Finance

appeared on behalf of the applicants for personal hearing on 5-2-2020 and they

reiterated the submissions already made in the application and Annexure with

the application and also submitted the written submission specifically mention-

ing the eligibility for exemption granted under Entry No. 3 of Notification No.

12/2017-C.T. (R), dated 28th June, 2017. They also sought to submit copies of cer-

tain documents and requested that the same may be taken on record. According-

ly, the documents submitted have been taken on record for consideration.

7. Discussions and findings :

7.1 We have carefully considered the submissions made by the appli-

cant in the application and also the documents submitted at the time of personal

hearing. In view of above deliberations and on considering the various docu-

ments furnished by the applicant following are the findings. We proceed to ex-

amine the questions applied for by the applicant.

7.2 Coming to the first question; Whether the amount recovered by the

applicant from other government departments for doing research work and

study, which help them make policies or understand its impact, chargeable to

GST? We need to dwell into the Exemption Notification No. 12/2017-C.T. (R),

dated 28th June, 2017.

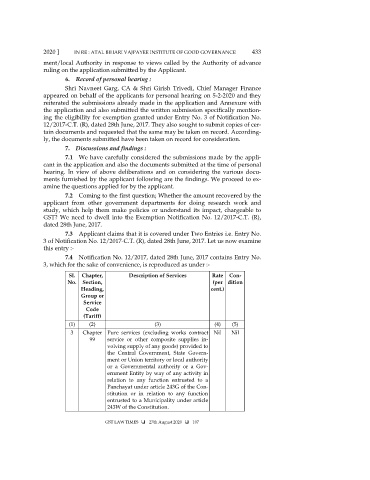

7.3 Applicant claims that it is covered under Two Entries i.e. Entry No.

3 of Notification No. 12/2017-C.T. (R), dated 28th June, 2017. Let us now examine

this entry :-

7.4 Notification No. 12/2017, dated 28th June, 2017 contains Entry No.

3, which for the sake of convenience, is reproduced as under :-

Sl. Chapter, Description of Services Rate Con-

No. Section, (per dition

Heading, cent.)

Group or

Service

Code

(Tariff)

(1) (2) (3) (4) (5)

3 Chapter Pure services (excluding works contract Nil Nil

99 service or other composite supplies in-

volving supply of any goods) provided to

the Central Government, State Govern-

ment or Union territory or local authority

or a Governmental authority or a Gov-

ernment Entity by way of any activity in

relation to any function entrusted to a

Panchayat under article 243G of the Con-

stitution or in relation to any function

entrusted to a Municipality under article

243W of the Constitution.

GST LAW TIMES 27th August 2020 107