Page 46 - GSTL_27th August 2020_Vol 39_Part 4

P. 46

J102 GST LAW TIMES [ Vol. 39

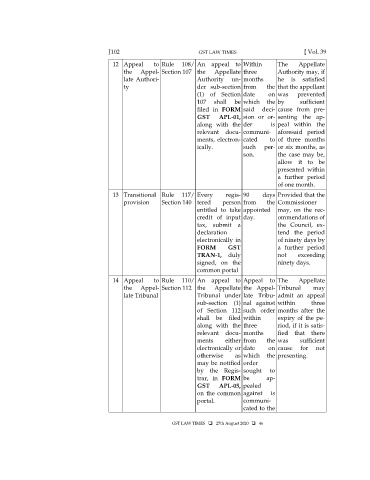

12 Appeal to Rule 108/ An appeal to Within The Appellate

the Appel- Section 107 the Appellate three Authority may, if

late Authori- Authority un- months he is satisfied

ty der sub-section from the that the appellant

(1) of Section date on was prevented

107 shall be which the by sufficient

filed in FORM said deci- cause from pre-

GST APL-01, sion or or- senting the ap-

along with the der is peal within the

relevant docu- communi- aforesaid period

ments, electron- cated to of three months

ically. such per- or six months, as

son. the case may be,

allow it to be

presented within

a further period

of one month.

13 Transitional Rule 117/ Every regis- 90 days Provided that the

provision Section 140 tered person from the Commissioner

entitled to take appointed may, on the rec-

credit of input day. ommendations of

tax, submit a the Council, ex-

declaration tend the period

electronically in of ninety days by

FORM GST a further period

TRAN-1, duly not exceeding

signed, on the ninety days.

common portal

14 Appeal to Rule 110/ An appeal to Appeal to The Appellate

the Appel- Section 112 the Appellate the Appel- Tribunal may

late Tribunal Tribunal under late Tribu- admit an appeal

sub-section (1) nal against within three

of Section 112 such order months after the

shall be filed within expiry of the pe-

along with the three riod, if it is satis-

relevant docu- months fied that there

ments either from the was sufficient

electronically or date on cause for not

otherwise as which the presenting.

may be notified order

by the Regis- sought to

trar, in FORM be ap-

GST APL-05, pealed

on the common against is

portal. communi-

cated to the

GST LAW TIMES 27th August 2020 46