Page 63 - GSTL_27th August 2020_Vol 39_Part 4

P. 63

2020 ] HITECH PROJECTS PVT. LTD. v. UNION OF INDIA 389

(E) An ex parte ad-interim relief in terms of prayer “B” above may kindly

be granted.”

2. The facts giving rise to this writ application may be summarized as

under :

2.1 The writ applicant No. 1 is a company engaged in the work of civil

construction since 1996-97. It appears from the materials on the record that a

Show Cause Notice No. V.38/15-54/OA/2016, dated 2-5-2016 was served upon

the writ applicants calling upon them to show cause as to why the Central Excise

duty amounting to Rs. 27,57,942/- for the period between April, 2011 and

31-12-2015 should not be recovered under Section 11A(4) of the Central Excise

Act, 1944. In other words, the writ applicants were called upon to show cause as

to why the RMC falling under the Central Excise Tariff Heading 3824 50 10

should not be demanded and recovered with interest. The writ applicants were

also called upon to show cause as to why the excisable goods valued at

Rs. 15,05,92,859/- should not be confiscated under Rule 25(2) of the Central

Excise Rules, 2002 and why the penalty under Rule 25(1) of Rules, 2002 read with

Section 11AC(1)(c) of the Act, 1944 should not be imposed.

2.2 The above referred show cause notice also proposed to impose pen-

alty on one of the partners of the firm viz. Shri Tejas Dalai under Rule 26 of the

Rules.

3. We need not go into any further details about the proceedings which

came to be initiated by the Department against the writ applicants in the year

2016 as we are of the view that this litigation can be put to an end by appropriate

directions to the respondents.

4. We may only observe that the show cause notice referred to above

ultimately came to be adjudicated and an order in original dated 13-4-2017 was

passed by the Assistant Commissioner, Central Excise, Division-V, Ahmedabad

confirming the demand of duty amounting to Rs. 27,57,942/- under Section

11A(4) of the Act, 1944 with interest under Section 11AA of the said Act. The rec-

ord further reveals that the adjudicating authority imposed redemption fine of

Rs. 5,00,000/- in lieu of the confiscation of the excisable goods valued at

Rs. 15,05,92,859/- manufactured and consumed by the writ applicants under Sec-

tion 34 of the Act, 1944.

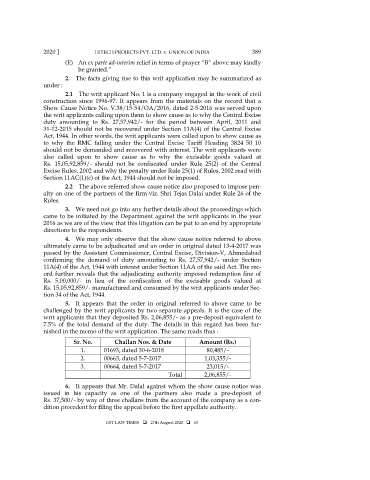

5. It appears that the order in original referred to above came to be

challenged by the writ applicants by two separate appeals. It is the case of the

writ applicants that they deposited Rs. 2,06,855/- as a pre-deposit equivalent to

7.5% of the total demand of the duty. The details in this regard has been fur-

nished in the memo of the writ application. The same reads thus :

Sr. No. Challan Nos. & Date Amount (Rs.)

1. 01693, dated 30-6-2018 80,485/-

2. 00663, dated 5-7-2017 1,03,355/-

3. 00664, dated 5-7-2017 23,015/-

Total 2,06,855/-

6. It appears that Mr. Dalal against whom the show cause notice was

issued in his capacity as one of the partners also made a pre-deposit of

Rs. 37,500/- by way of three challans from the account of the company as a con-

dition precedent for filing the appeal before the first appellate authority.

GST LAW TIMES 27th August 2020 63