Page 79 - GSTL_27th August 2020_Vol 39_Part 4

P. 79

2020 ] IN RE : APAR INDUSTRIES LTD. 405

groups goods into Six Schedules for the purpose of uniformity in levying and

affixing rate of GST category-wise/schedule-wise. All Goods of Schedule-I are

categorized as 5% GST rated goods, wherein Sr. No. 250 and 252 refers to the fol-

lowing supply/goods -

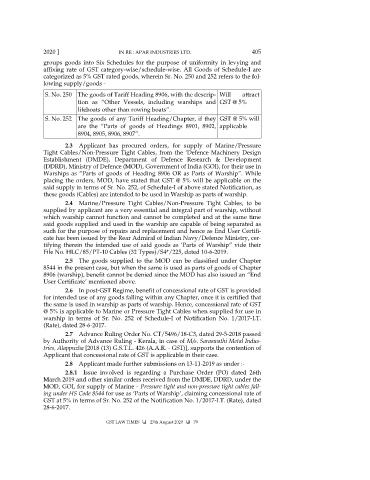

S. No. 250 The goods of Tariff Heading 8906, with the descrip- Will attract

tion as “Other Vessels, including warships and GST @ 5%

lifeboats other than rowing boats”.

S. No. 252 The goods of any Tariff Heading/Chapter, if they GST @ 5% will

are the “Parts of goods of Headings 8901, 8902, applicable

8904, 8905, 8906, 8907”.

2.3 Applicant has procured orders, for supply of Marine/Pressure

Tight Cables/Non-Pressure Tight Cables, from the ‘Defence Machinery Design

Establishment (DMDE), Department of Defence Research & Development

(DDRD), Ministry of Defence (MOD), Government of India (GOI), for their use in

Warships as “Parts of goods of Heading 8906 OR as Parts of Warship”. While

placing the orders, MOD, have stated that GST @ 5% will be applicable on the

said supply in terms of Sr. No. 252, of Schedule-I of above stated Notification, as

these goods (Cables) are intended to be used in Warship as parts of warship.

2.4 Marine/Pressure Tight Cables/Non-Pressure Tight Cables, to be

supplied by applicant are a very essential and integral part of warship, without

which warship cannot function and cannot be completed and at the same time

said goods supplied and used in the warship are capable of being separated as

such for the purpose of repairs and replacement and hence as End User Certifi-

cate has been issued by the Rear Admiral of Indian Navy/Defence Ministry, cer-

tifying therein the intended use of said goods as ‘Parts of Warship” vide their

File No. HLC/85/PT-10 Cables (32 Types)/S4*/225, dated 10-6-2019.

2.5 The goods supplied to the MOD can be classified under Chapter

8544 in the present case, but when the same is used as parts of goods of Chapter

8906 (warship), benefit cannot be denied since the MOD has also issued an “End

User Certificate’ mentioned above.

2.6 In post-GST Regime, benefit of concessional rate of GST is provided

for intended use of any goods falling within any Chapter, once it is certified that

the same is used in warship as parts of warship. Hence, concessional rate of GST

@ 5% is applicable to Marine or Pressure Tight Cables when supplied for use in

warship in terms of Sr. No. 252 of Schedule-I of Notification No. 1/2017-I.T.

(Rate), dated 28-6-2017.

2.7 Advance Ruling Order No. CT/5496/18-C3, dated 29-5-2018 passed

by Authority of Advance Ruling - Kerala, in case of M/s. Saraswathi Metal Indus-

tries, Alappuzha [2018 (13) G.S.T.L. 426 (A.A.R. - GST)], supports the contention of

Applicant that concessional rate of GST is applicable in their case.

2.8 Applicant made further submissions on 13-11-2019 as under :-

2.8.1 Issue involved is regarding a Purchase Order (PO) dated 26th

March 2019 and other similar orders received from the DMDE, DDRD, under the

MOD, GOI, for supply of Marine - Pressure tight and non-pressure tight cables fall-

ing under HS Code 8544 for use as ‘Parts of Warship’, claiming concessional rate of

GST at 5% in terms of Sr. No. 252 of the Notification No. 1/2017-I.T. (Rate), dated

28-6-2017.

GST LAW TIMES 27th August 2020 79