Page 229 - ELT_1_1st April 2020_Vol 372_Part

P. 229

2020 ] HIM LOGISTICS PVT. LTD. v. COMMR. OF CUS., NEW DELHI ICD TKD EXPORT 115

12. It further appeared that the value of food supplements containing

beef cannot be determined under Rule 4 or 5 of the Valuation Rules as import of

beef in any form and import of products containing beef in any form is prohibit-

ed. In absence of identical or similar goods, the value was proposed to be deter-

mined in terms of Rule 7 (deductive value) taking into account the maximum

retail price offered by e-retailer M/s. Amazon, for similar food supplements, and

after allowing deduction towards transport cost, insurance cost, customs duty,

reasonable profits margins, etc. Taking the MRP (per unit price) from the inter-

net, valuation was done, giving rebate of 35% on MRP, working the assessable

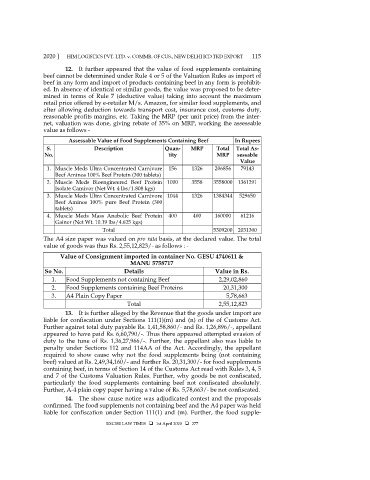

value as follows -

Assessable Value of Food Supplements Containing Beef In Rupees

S. Description Quan- MRP Total Total As-

No. tity MRP sessable

Value

1. Muscle Meds Ultra Concentrated Carnivore 156 1326 206856 79143

Beef Aminos 100% Beef Protein (300 tablets)

2. Muscle Meds Bioengineered Beef Protein 1000 3558 3558000 1361291

Isolate Camivor (Net Wt. 4 lbs/1.808 kgs)

3. Muscle Meds Ultra Concentrated Carnivore 1044 1326 1384344 529650

Beef Aminos 100% pure Beef Protein (300

tablets)

4. Muscle Meds Mass Anabolic Beef Protein 400 400 160000 61216

Gainer (Net Wt. 10.19 lbs/4.625 kgs)

Total 5309200 2031300

The A4 size paper was valued on pro rata basis, at the declared value. The total

value of goods was thus Rs. 2,55,12,823/- as follows : -

Value of Consignment imported in container No. GESU 4740611 &

MANU 5758717

So No. Details Value in Rs.

1. Food Supplements not containing Beef 2,29,02,860

2. Food Supplements containing Beef Proteins 20,31,300

3. A4 Plain Copy Paper 5,78,663

Total 2,55,12,823

13. It is further alleged by the Revenue that the goods under import are

liable for confiscation under Sections 111(1)(m) and (n) of the of Customs Act.

Further against total duty payable Rs. 1,41,58,860/- and Rs. 1,26,896/-, appellant

appeared to have paid Rs. 6,60,790/-. Thus there appeared attempted evasion of

duty to the tune of Rs. 1,36,27,966/-. Further, the appellant also was liable to

penalty under Sections 112 and 114AA of the Act. Accordingly, the appellant

required to show cause why not the food supplements being (not containing

beef) valued at Rs. 2,49,34,160/- and further Rs. 20,31,300/- for food supplements

containing beef, in terms of Section 14 of the Customs Act read with Rules 3, 4, 5

and 7 of the Customs Valuation Rules. Further, why goods be not confiscated,

particularly the food supplements containing beef not confiscated absolutely.

Further, A-4 plain copy paper having a value of Rs. 5,78,663/- be not confiscated.

14. The show cause notice was adjudicated contest and the proposals

confirmed. The food supplements not containing beef and the A4 paper was held

liable for confiscation under Section 111(1) and (m). Further, the food supple-

EXCISE LAW TIMES 1st April 2020 277