Page 232 - ELT_1_1st April 2020_Vol 372_Part

P. 232

118 EXCISE LAW TIMES [ Vol. 372

thus at the gross value determined by the Department at Rs. 2,29,03,044/-, will

be as reduced by 40%, the value is worked out at Rs. 1,37,41,826/-.

Further on the above value, their duty payable will be Rs. 74,04,305/-

(approx.).

21. The Ld. Counsel for the appellant further submits that the value of

the goods is taken as per data which is showing the value of USA origin goods.

Since, the goods imported are of Chinese origin, they will be having some lesser

value. Still the Ld. Counsel for the appellant is calculating rebate @ 40% on the

value of Rs. 2,29,03,044/- as per Rule 7 of Customs Valuation Rules, 2007. The

value calculated is as follows :-

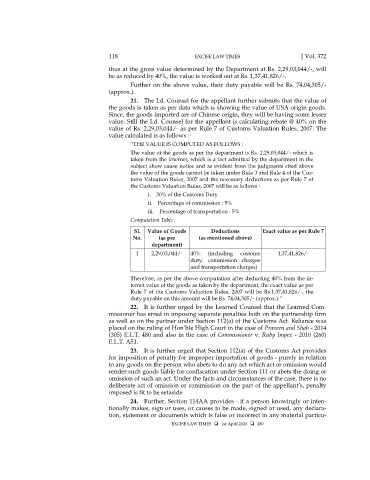

“THE VALUE IS COMPUTED AS FOLLOWS :

The value of the goods as per the department is Rs. 2,29,03,044/- which is

taken from the internet, which is a fact admitted by the department in the

subject show cause notice and as evident from the judgments cited above

the value of the goods cannot be taken under Rule 3 and Rule 4 of the Cus-

toms Valuation Rules, 2007 and the necessary deductions as per Rule 7 of

the Customs Valuation Rules, 2007 will be as follows :

i. 30% of the Customs Duty

ii. Percentage of commission : 5%

iii. Percentage of transportation : 5%

Computation Table :

Sl. Value of Goods Deductions Exact value as per Rule 7

No. (as per (as mentioned above)

department)

1 2,29,03,044/- 40% (including customs 1,37,41,826/-

duty, commission charges

and transportation charges)

Therefore, as per the above computation after deducting 40% from the in-

ternet value of the goods as taken by the department, the exact value as per

Rule 7 of the Customs Valuation Rules, 2007 will be Rs.1,37,41,826/-, the

duty payable on this amount will be Rs. 74,04,305/- (approx.).”

22. It is further urged by the Learned Counsel that the Learned Com-

missioner has erred in imposing separate penalties both on the partnership firm

as well as on the partner under Section 112(a) of the Customs Act. Reliance was

placed on the ruling of Hon’ble High Court in the case of Praveen and Shah - 2014

(305) E.L.T. 480 and also in the case of Commissioner v. Ruby Impex - 2010 (260)

E.L.T. A51.

23. It is further urged that Section 112(a) of the Customs Act provides

for imposition of penalty for improper importation of goods - purely in relation

to any goods on the person who abets to do any act which act or omission would

render such goods liable for confiscation under Section 111 or abets the doing or

omission of such an act. Under the facts and circumstances of the case, there is no

deliberate act of omission or commission on the part of the appellant’s, penalty

imposed is fit to be setaside

24. Further, Section 114AA provides - if a person knowingly or inten-

tionally makes, sign or uses, or causes to be made, signed or used, any declara-

tion, statement or documents which is false or incorrect in any material particu-

EXCISE LAW TIMES 1st April 2020 280