Page 214 - ELT_2nd_15th April 2020_Vol 372_Part

P. 214

260 EXCISE LAW TIMES [ Vol. 372

placed on the decision of M/s. Siddachalam Export Private Limited v. Commissioner

of Central Excise, Delhi-III; [2011 (267) E.L.T. 3 (S.C.)]. Further, Learned Advocate

also relied upon the decision of the Hon’ble High Court in the case of Commis-

sioner of Customs, New Delhi v. Vishal Exports Overseas Limited, [2007 (209) E.L.T.

331 (S.C.)] regarding acceptance of FOB value, which was supported by the Bank

Realisation Certificate (BRC). The Present Market Value (PMV) was also not ob-

tained by the Department which is not legally correct. In the circumstances,

Learned Advocate submitted that no case is made out for the misdeclaration of

the export consignment and therefore confiscating the export goods and imposi-

tion of redemption fine is illegal, and also on the director of the company is also

not sustainable.

11. Learned Departmental Representative supports the finding con-

tained in the impugned order.

12. We have heard Learned Advocate appearing on behalf of the Ap-

pellant and Learned Departmental Representative on behalf of the Revenue. The

issue to be decided in this appeal is as to whether the appellant has misdeclared

the export consignment in respect of value thereof, which as per the department

is highly inflated. The department has solely relied upon the report obtained

from the CSIR-CLRI regarding composition and price of the export consignment.

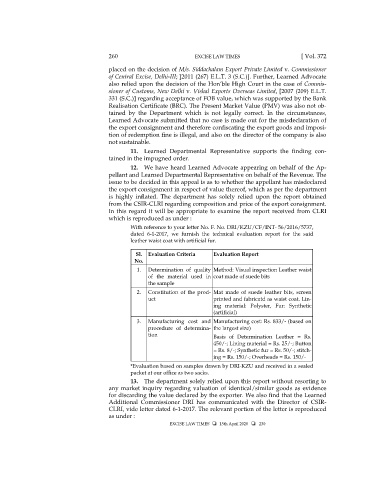

In this regard it will be appropriate to examine the report received from CLRI

which is reproduced as under :

With reference to your letter No. F. No. DRI/KZU/CF/INT- 56/2016/5737,

dated 6-1-2017, we furnish the technical evaluation report for the said

leather waist coat with artificial fur.

Sl. Evaluation Criteria Evaluation Report

No.

1. Determination of quality Method: Visual inspection Leather waist

of the material used in coat made of suede bits

the sample

2. Constitution of the prod- Mat made of suede leather bits, screen

uct printed and fabricatd as waist coat. Lin-

ing material: Polyster, Fur: Synthetic

(artificial)

3. Manufacturing cost and Manufacturing cost: Rs. 833/- (based on

procedure of determina- the largest size)

tion Basis of Determination Leather = Rs.

450/-; Lining material = Rs. 25/-; Button

= Rs. 8/-; Synthetic fur = Rs. 50/-; stitch-

ing = Rs. 150/-; Overheads = Rs. 150/-

*Evaluation based on samples drawn by DRI-KZU and received in a sealed

packet at our office as two sacks.

13. The department solely relied upon this report without resorting to

any market inquiry regarding valuation of identical/similar goods as evidence

for discarding the value declared by the exporter. We also find that the Learned

Additional Commissioner DRI has communicated with the Director of CSIR-

CLRI, vide letter dated 6-1-2017. The relevant portion of the letter is reproduced

as under :

EXCISE LAW TIMES 15th April 2020 230