Page 239 - ELT_2nd_15th April 2020_Vol 372_Part

P. 239

2020 ] PEE CEE COSMA SOPE LTD. v. COMMISSIONER OF CENTRAL EXCISE, KANPUR 285

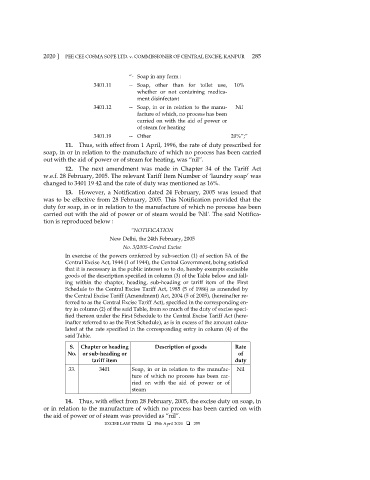

“- Soap in any form :

3401.11 -- Soap, other than for toilet use, 10%

whether or not containing medica-

ment disinfectant

3401.12 -- Soap, in or in relation to the manu- Nil

facture of which, no process has been

carried on with the aid of power or

of steam for heating

3401.19 -- Other 20%”;”

11. Thus, with effect from 1 April, 1996, the rate of duty prescribed for

soap, in or in relation to the manufacture of which no process has been carried

out with the aid of power or of steam for heating, was “nil”.

12. The next amendment was made in Chapter 34 of the Tariff Act

w.e.f. 28 February, 2005. The relevant Tariff Item Number of ‘laundry soap’ was

changed to 3401 19 42 and the rate of duty was mentioned as 16%.

13. However, a Notification dated 24 February, 2005 was issued that

was to be effective from 28 February, 2005. This Notification provided that the

duty for soap, in or in relation to the manufacture of which no process has been

carried out with the aid of power or of steam would be 'Nil'. The said Notifica-

tion is reproduced below :

“NOTIFICATION

New Delhi, the 24th February, 2005

No. 3/2005-Central Excise

In exercise of the powers conferred by sub-section (1) of section 5A of the

Central Excise Act, 1944 (1 of 1944), the Central Government, being satisfied

that it is necessary in the public interest so to do, hereby exempts excisable

goods of the description specified in column (3) of the Table below and fall-

ing within the chapter, heading, sub-heading or tariff item of the First

Schedule to the Central Excise Tariff Act, 1985 (5 of 1986) as amended by

the Central Excise Tariff (Amendment) Act, 2004 (5 of 2005), (hereinafter re-

ferred to as the Central Excise Tariff Act), specified in the corresponding en-

try in column (2) of the said Table, from so much of the duty of excise speci-

fied thereon under the First Schedule to the Central Excise Tariff Act (here-

inafter referred to as the First Schedule), as is in excess of the amount calcu-

lated at the rate specified in the corresponding entry in column (4) of the

said Table.

S. Chapter or heading Description of goods Rate

No. or sub-heading or of

tariff item duty

33. 3401 Soap, in or in relation to the manufac- Nil

ture of which no process has been car-

ried on with the aid of power or of

steam

14. Thus, with effect from 28 February, 2005, the excise duty on soap, in

or in relation to the manufacture of which no process has been carried on with

the aid of power or of steam was provided as “nil”.

EXCISE LAW TIMES 15th April 2020 255