Page 102 - GSTL_30th April 2020_Vol 35_Part 5

P. 102

588 GST LAW TIMES [ Vol. 35

vices Tax Act, 2017 & Rajasthan Goods and Service Tax Act, 2017 shall be

paid on reverse charge basis by the recipient of the such services”. The noti-

fication is issued under Section 9(3) of the CGST Act, 2017. Entry 6 of the

said Notification reads as under -

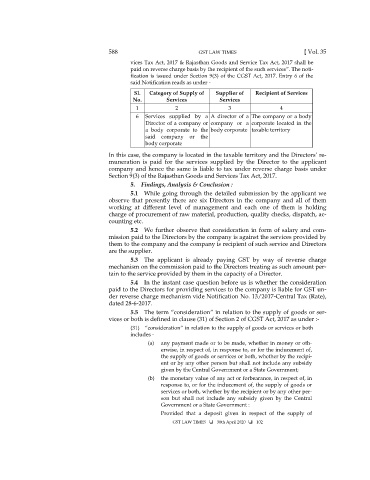

Sl. Category of Supply of Supplier of Recipient of Services

No. Services Services

1 2 3 4

6 Services supplied by a A director of a The company or a body

Director of a company or company or a corporate located in the

a body corporate to the body corporate taxable territory

said company or the

body corporate

In this case, the company is located in the taxable territory and the Directors’ re-

muneration is paid for the services supplied by the Director to the applicant

company and hence the same is liable to tax under reverse charge basis under

Section 9(3) of the Rajasthan Goods and Services Tax Act, 2017.

5. Findings, Analysis & Conclusion :

5.1 While going through the detailed submission by the applicant we

observe that presently there are six Directors in the company and all of them

working at different level of management and each one of them is holding

charge of procurement of raw material, production, quality checks, dispatch, ac-

counting etc.

5.2 We further observe that consideration in form of salary and com-

mission paid to the Directors by the company is against the services provided by

them to the company and the company is recipient of such service and Directors

are the supplier.

5.3 The applicant is already paying GST by way of reverse charge

mechanism on the commission paid to the Directors treating as such amount per-

tain to the service provided by them in the capacity of a Director.

5.4 In the instant case question before us is whether the consideration

paid to the Directors for providing services to the company is liable for GST un-

der reverse charge mechanism vide Notification No. 13/2017-Central Tax (Rate),

dated 28-6-2017.

5.5 The term “consideration” in relation to the supply of goods or ser-

vices or both is defined in clause (31) of Section 2 of CGST Act, 2017 as under :-

(31) “consideration” in relation to the supply of goods or services or both

includes -

(a) any payment made or to be made, whether in money or oth-

erwise, in respect of, in response to, or for the inducement of,

the supply of goods or services or both, whether by the recipi-

ent or by any other person but shall not include any subsidy

given by the Central Government or a State Government;

(b) the monetary value of any act or forbearance, in respect of, in

response to, or for the inducement of, the supply of goods or

services or both, whether by the recipient or by any other per-

son but shall not include any subsidy given by the Central

Government or a State Government :

Provided that a deposit given in respect of the supply of

GST LAW TIMES 30th April 2020 102