Page 103 - GSTL_30th April 2020_Vol 35_Part 5

P. 103

2020 ] IN RE : CLAY CRAFT INDIA PVT. LTD. 589

goods or services or both shall not be considered as payment

made for such supply unless the supplier applies such deposit

as consideration for the said supply;”

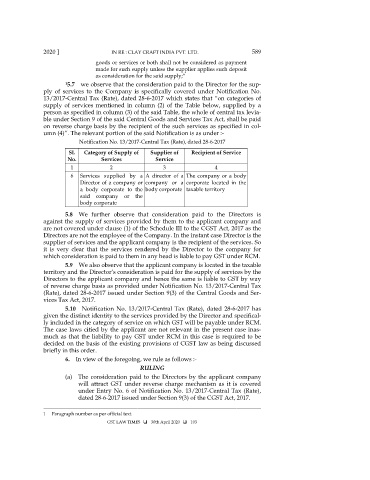

1 5.7 we observe that the consideration paid to the Director for the sup-

ply of services to the Company is specifically covered under Notification No.

13/2017-Central Tax (Rate), dated 28-6-2017 which states that “on categories of

supply of services mentioned in column (2) of the Table below, supplied by a

person as specified in column (3) of the said Table, the whole of central tax levia-

ble under Section 9 of the said Central Goods and Services Tax Act, shall be paid

on reverse charge basis by the recipient of the such services as specified in col-

umn (4)”. The relevant portion of the said Notification is as under :-

Notification No. 13/2017-Central Tax (Rate), dated 28-6-2017

Sl. Category of Supply of Supplier of Recipient of Service

No. Services Service

1 2 3 4

6 Services supplied by a A director of a The company or a body

Director of a company or company or a corporate located in the

a body corporate to the body corporate taxable territory

said company or the

body corporate

5.8 We further observe that consideration paid to the Directors is

against the supply of services provided by them to the applicant company and

are not covered under clause (1) of the Schedule III to the CGST Act, 2017 as the

Directors are not the employee of the Company. In the instant case Director is the

supplier of services and the applicant company is the recipient of the services. So

it is very clear that the services rendered by the Director to the company for

which consideration is paid to them in any head is liable to pay GST under RCM.

5.9 We also observe that the applicant company is located in the taxable

territory and the Director’s consideration is paid for the supply of services by the

Directors to the applicant company and hence the same is liable to GST by way

of reverse charge basis as provided under Notification No. 13/2017-Central Tax

(Rate), dated 28-6-2017 issued under Section 9(3) of the Central Goods and Ser-

vices Tax Act, 2017.

5.10 Notification No. 13/2017-Central Tax (Rate), dated 28-6-2017 has

given the distinct identity to the services provided by the Director and specifical-

ly included in the category of service on which GST will be payable under RCM.

The case laws citied by the applicant are not relevant in the present case inas-

much as that the liability to pay GST under RCM in this case is required to be

decided on the basis of the existing provisions of CGST law as being discussed

briefly in this order.

6. In view of the foregoing, we rule as follows :-

RULING

(a) The consideration paid to the Directors by the applicant company

will attract GST under reverse charge mechanism as it is covered

under Entry No. 6 of Notification No. 13/2017-Central Tax (Rate),

dated 28-6-2017 issued under Section 9(3) of the CGST Act, 2017.

________________________________________________________________________

1 Paragraph number as per official text.

GST LAW TIMES 30th April 2020 103