Page 108 - GSTL_30th April 2020_Vol 35_Part 5

P. 108

594 GST LAW TIMES [ Vol. 35

6.1 The applicant seeks Advance Ruling as to whether royalty paid in

respect of Mining Lease can be classified under “Licensing services for the right to

use minerals including its exploration and evaluation” falling under the SAC 9973

and what is the rate of GST on the said supply. Further, Section 9B and 9C of the

‘Mines and Minerals (Development & Regulation) Act, 1957 mandates that the

miners shall contribute 30% of the royalty amount paid to the Government, to

the District Mineral Foundation and 2% of the royalty amount to the ‘National

Mineral Exploration Trust’. In this context the applicant seeks Advance Ruling as

to whether the contribution/payment made to the funds can be treated as con-

sideration against supply and whether the same is subject to levy of GST under

Reverse Charge.

7. Royalty is required to be paid as per Section 9(1) of the Mines and

Mineral (Development and Regulation) Act, 1957, which reads as under :

“The holder of a mining lease granted shall, notwithstanding anything con-

tained in the instrument of lease or in any law in force at such commence-

ment, pay royalty in respect of any [mineral removed or consumed by him

or by his agent, manager, employee, contractor or sub-lessee] from the

leased area after such commencement, at the rate for the time being speci-

fied in the Second Schedule in respect of that minerals.”

7.1 The Central Board of Indirect Taxes and Customs (CBIC) in Sectoral

FAQ’s has clarifies that the royalty payment is made towards Licensing services

for exploration of natural resources. The extract of the same is reproduced as un-

der :

“The Government provides license to various companies including Public

Sector Undertakings for exploration of natural resources like oil, hydrocar-

bons, iron ore, manganese, etc. For having assigned the rights to use the

natural resources, the licensee companies are required to pay consideration

in the form of annual license fee, lease charges, royalty, etc. to the Govern-

ment. The activity of assignment of rights to use natural resources is treated

as supply of services and the licensee is required to pay tax on the amount of

consideration paid in the form of royalty or any other form under reverse charge

mechanism.”

7.2 The note on ‘Mineral Royalties’ published by the Indian Bureau of

Mines is reproduced as under :

“A lessee is a person who is granted mineral concessions. The lessee is re-

quired to pay a certain amount in respect of the mineral extracted in pro-

portion to the quantity extracted. Such payment is called royalty. The royal-

ties in respect of mining leases is specified in Section 9 of the Mines and

Mineral (Development and Regulation) Act, 1957. Royalty is a variable re-

turn and it varies with the quantity of minerals extracted or removed.”

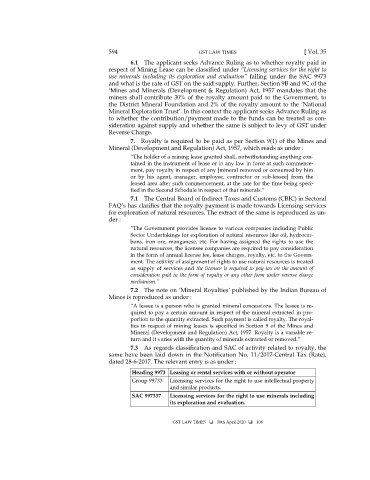

7.3 As regards classification and SAC of activity related to royalty, the

same have been laid down in the Notification No. 11/2017-Central Tax (Rate),

dated 28-6-2017. The relevant entry is as under :

Heading 9973 Leasing or rental services with or without operator

Group 99733 Licensing services for the right to use intellectual property

and similar products.

SAC 997337 Licensing services for the right to use minerals including

its exploration and evaluation.

GST LAW TIMES 30th April 2020 108