Page 150 - GSTL_30th April 2020_Vol 35_Part 5

P. 150

636 GST LAW TIMES [ Vol. 35

which are related to different issues. In all these questions the applicant raises

same type of question whether the activity in these different issues amounts to

supply of goods or services. These questions have been already answered in the

relevant issues and hence they are redundant.

12. In view of the foregoing, we pass the following

RULING

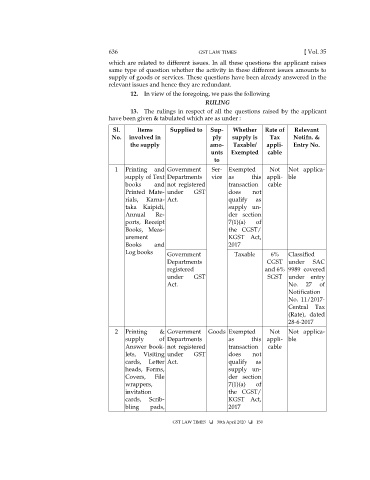

13. The rulings in respect of all the questions raised by the applicant

have been given & tabulated which are as under :

Sl. Items Supplied to Sup- Whether Rate of Relevant

No. involved in ply supply is Tax Notifn. &

the supply amo- Taxable/ appli- Entry No.

unts Exempted cable

to

1 Printing and Government Ser- Exempted Not Not applica-

supply of Text Departments vice as this appli- ble

books and not registered transaction cable

Printed Mate- under GST does not

rials, Karna- Act. qualify as

taka Kaipidi, supply un-

Annual Re- der section

ports, Receipt 7(1)(a) of

Books, Meas- the CGST/

urement KGST Act,

Books and 2017

Log books Government Taxable 6% Classified

Departments CGST under SAC

registered and 6% 9989 covered

under GST SGST under entry

Act. No. 27 of

Notification

No. 11/2017-

Central Tax

(Rate), dated

28-6-2017

2 Printing & Government Goods Exempted Not Not applica-

supply of Departments as this appli- ble

Answer book- not registered transaction cable

lets, Visiting under GST does not

cards, Letter Act. qualify as

heads, Forms, supply un-

Covers, File der section

wrappers, 7(1)(a) of

invitation the CGST/

cards, Scrib- KGST Act,

bling pads, 2017

GST LAW TIMES 30th April 2020 150