Page 23 - GSTL_30th April 2020_Vol 35_Part 5

P. 23

2020 ] ANALYSIS OF RELIEF MEASURES PROVIDED UNDER GST LAW DUE TO COVID-19 J75

ANALYSIS OF RELIEF MEASURES PROVIDED UNDER GST LAW DUE TO COVID-19

ANALYSIS OF RELIEF MEASURES PROVIDED UNDER GST

LAW DUE TO COVID-19 OUTBREAK

ANALYSIS OF RELIEF MEASURES PROVIDED UNDER GST LAW DUE TO COVID-19

By

Shuchi Agrawal

ALA LEGAL, ADVOCATES & SOLICITORS

CBIC has in view of the emergent situations being faced by taxpayers on

account of Corona Virus outbreak issued various relief measures relating to stat-

utory and regulatory compliance matters under various provisions of GST Law.

A brief analysis of the Notification Nos. 30/2020 to 36/2020, dated 3-4-2020 are

summarized here under :

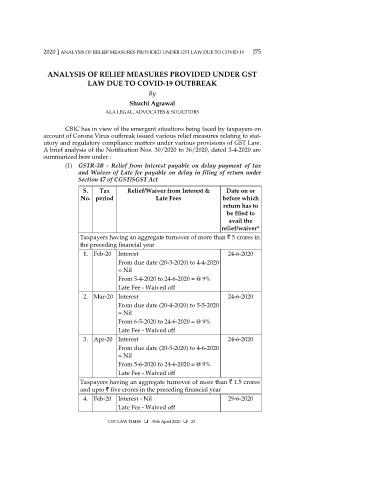

(1) GSTR-3B - Relief from Interest payable on delay payment of tax

and Waiver of Late fee payable on delay in filing of return under

Section 47 of CGST/SGST Act

S. Tax Relief/Waiver from Interest & Date on or

No. period Late Fees before which

return has to

be filed to

avail the

relief/waiver*

Taxpayers having an aggregate turnover of more than ` 5 crores in

the preceding financial year

1. Feb-20 Interest 24-6-2020

From due date (20-3-2020) to 4-4-2020

= Nil

From 5-4-2020 to 24-6-2020 = @ 9%

Late Fee - Waived off

2. Mar-20 Interest 24-6-2020

From due date (20-4-2020) to 5-5-2020

= Nil

From 6-5-2020 to 24-6-2020 = @ 9%

Late Fee - Waived off

3. Apr-20 Interest 24-6-2020

From due date (20-5-2020) to 4-6-2020

= Nil

From 5-6-2020 to 24-6-2020 = @ 9%

Late Fee - Waived off

Taxpayers having an aggregate turnover of more than ` 1.5 crores

and upto ` five crores in the preceding financial year

4. Feb-20 Interest - Nil 29-6-2020

Late Fee - Waived off

GST LAW TIMES 30th April 2020 23