Page 25 - GSTL_30th April 2020_Vol 35_Part 5

P. 25

2020 ] ANALYSIS OF RELIEF MEASURES PROVIDED UNDER GST LAW DUE TO COVID-19 J77

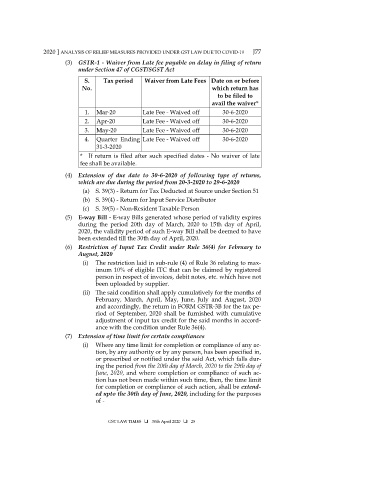

(3) GSTR-1 - Waiver from Late fee payable on delay in filing of return

under Section 47 of CGST/SGST Act

S. Tax period Waiver from Late Fees Date on or before

No. which return has

to be filed to

avail the waiver*

1. Mar-20 Late Fee - Waived off 30-6-2020

2. Apr-20 Late Fee - Waived off 30-6-2020

3. May-20 Late Fee - Waived off 30-6-2020

4. Quarter Ending Late Fee - Waived off 30-6-2020

31-3-2020

* If return is filed after such specified dates - No waiver of late

fee shall be available.

(4) Extension of due date to 30-6-2020 of following type of returns,

which are due during the period from 20-3-2020 to 29-6-2020

(a) S. 39(3) - Return for Tax Deducted at Source under Section 51

(b) S. 39(4) - Return for Input Service Distributor

(c) S. 39(5) - Non-Resident Taxable Person

(5) E-way Bill - E-way Bills generated whose period of validity expires

during the period 20th day of March, 2020 to 15th day of April,

2020, the validity period of such E-way Bill shall be deemed to have

been extended till the 30th day of April, 2020.

(6) Restriction of Input Tax Credit under Rule 36(4) for February to

August, 2020

(i) The restriction laid in sub-rule (4) of Rule 36 relating to max-

imum 10% of eligible ITC that can be claimed by registered

person in respect of invoices, debit notes, etc. which have not

been uploaded by supplier.

(ii) The said condition shall apply cumulatively for the months of

February, March, April, May, June, July and August, 2020

and accordingly, the return in FORM GSTR-3B for the tax pe-

riod of September, 2020 shall be furnished with cumulative

adjustment of input tax credit for the said months in accord-

ance with the condition under Rule 36(4).

(7) Extension of time limit for certain compliances

(i) Where any time limit for completion or compliance of any ac-

tion, by any authority or by any person, has been specified in,

or prescribed or notified under the said Act, which falls dur-

ing the period from the 20th day of March, 2020 to the 29th day of

June, 2020, and where completion or compliance of such ac-

tion has not been made within such time, then, the time limit

for completion or compliance of such action, shall be extend-

ed upto the 30th day of June, 2020, including for the purposes

of -

GST LAW TIMES 30th April 2020 25