Page 154 - GSTL_7th May 2020_Vol 36_Part 1

P. 154

112 GST LAW TIMES [ Vol. 36

from tax under the GST Acts and therefore also no registration is required by

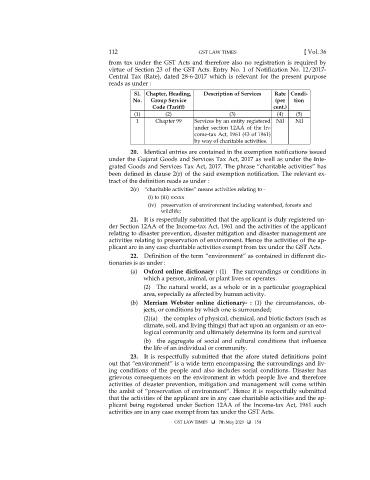

virtue of Section 23 of the GST Acts. Entry No. 1 of Notification No. 12/2017-

Central Tax (Rate), dated 28-6-2017 which is relevant for the present purpose

reads as under :

Sl. Chapter, Heading, Description of Services Rate Condi-

No. Group Service (per tion

Code (Tariff) cent.)

(1) (2) (3) (4) (5)

1 Chapter 99 Services by an entity registered Nil Nil

under section 12AA of the In-

come-tax Act, 1961 (43 of 1961)

by way of charitable activities.

20. Identical entries are contained in the exemption notifications issued

under the Gujarat Goods and Services Tax Act, 2017 as well as under the Inte-

grated Goods and Services Tax Act, 2017. The phrase “charitable activities” has

been defined in clause 2(r) of the said exemption notification. The relevant ex-

tract of the definition reads as under :

2(r) “charitable activities” means activities relating to -

(i) to (iii) xxxxx

(iv) preservation of environment including watershed, forests and

wildlife;

21. It is respectfully submitted that the applicant is duly registered un-

der Section 12AA of the Income-tax Act, 1961 and the activities of the applicant

relating to disaster prevention, disaster mitigation and disaster management are

activities relating to preservation of environment. Hence the activities of the ap-

plicant are in any case charitable activities exempt from tax under the GST Acts.

22. Definition of the term “environment” as contained in different dic-

tionaries is as under :

(a) Oxford online dictionary : (1) The surroundings or conditions in

which a person, animal, or plant lives or operates.

(2) The natural world, as a whole or in a particular geographical

area, especially as affected by human activity.

(b) Merriam Webster online dictionary- : (1) the circumstances, ob-

jects, or conditions by which one is surrounded;

(2)(a) the complex of physical, chemical, and biotic factors (such as

climate, soil, and living things) that act upon an organism or an eco-

logical community and ultimately determine its form and survival

(b) the aggregate of social and cultural conditions that influence

the life of an individual or community.

23. It is respectfully submitted that the afore stated definitions point

out that “environment” is a wide term encompassing the surroundings and liv-

ing conditions of the people and also includes social conditions. Disaster has

grievous consequences on the environment in which people live and therefore

activities of disaster prevention, mitigation and management will come within

the ambit of “preservation of environment”. Hence it is respectfully submitted

that the activities of the applicant are in any case charitable activities and the ap-

plicant being registered under Section 12AA of the Income-tax Act, 1961 such

activities are in any case exempt from tax under the GST Acts.

GST LAW TIMES 7th May 2020 154