Page 155 - GSTL_7th May 2020_Vol 36_Part 1

P. 155

2020 ] IN RE : ALL INDIA DISASTER MITIGATION INSTITUTE 113

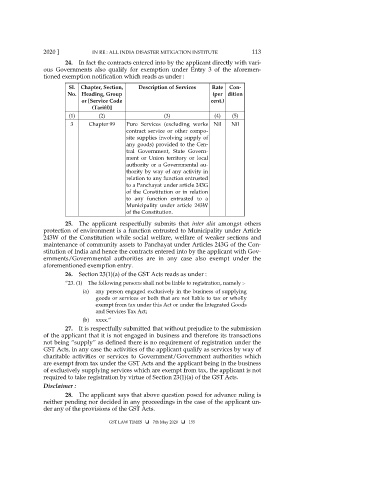

24. In fact the contracts entered into by the applicant directly with vari-

ous Governments also qualify for exemption under Entry 3 of the aforemen-

tioned exemption notification which reads as under :

Sl. Chapter, Section, Description of Services Rate Con-

No. Heading, Group (per dition

or [Service Code cent.)

(Tariff)]

(1) (2) (3) (4) (5)

3 Chapter 99 Pure Services (excluding works Nil Nil

contract service or other compo-

site supplies involving supply of

any goods) provided to the Cen-

tral Government, State Govern-

ment or Union territory or local

authority or a Governmental au-

thority by way of any activity in

relation to any function entrusted

to a Panchayat under article 243G

of the Constitution or in relation

to any function entrusted to a

Municipality under article 243W

of the Constitution.

25. The applicant respectfully submits that inter alia amongst others

protection of environment is a function entrusted to Municipality under Article

243W of the Constitution while social welfare, welfare of weaker sections and

maintenance of community assets to Panchayat under Articles 243G of the Con-

stitution of India and hence the contracts entered into by the applicant with Gov-

ernments/Governmental authorities are in any case also exempt under the

aforementioned exemption entry.

26. Section 23(1)(a) of the GST Acts reads as under :

“23. (1) The following persons shall not be liable to registration, namely :-

(a) any person engaged exclusively in the business of supplying

goods or services or both that are not liable to tax or wholly

exempt from tax under this Act or under the Integrated Goods

and Services Tax Act;

(b) xxxx.”

27. It is respectfully submitted that without prejudice to the submission

of the applicant that it is not engaged in business and therefore its transactions

not being “supply” as defined there is no requirement of registration under the

GST Acts, in any case the activities of the applicant qualify as services by way of

charitable activities or services to Government/Government authorities which

are exempt from tax under the GST Acts and the applicant being in the business

of exclusively supplying services which are exempt from tax, the applicant is not

required to take registration by virtue of Section 23(1)(a) of the GST Acts.

Disclaimer :

28. The applicant says that above question posed for advance ruling is

neither pending nor decided in any proceedings in the case of the applicant un-

der any of the provisions of the GST Acts.

GST LAW TIMES 7th May 2020 155