Page 117 - GSTL_11th June 2020_Vol 37_Part 2

P. 117

2020 ] SGS CONSTRUCTION & DEVELOPERS PVT. LTD. v. COMMR. OF S.T., NEW DELHI 203

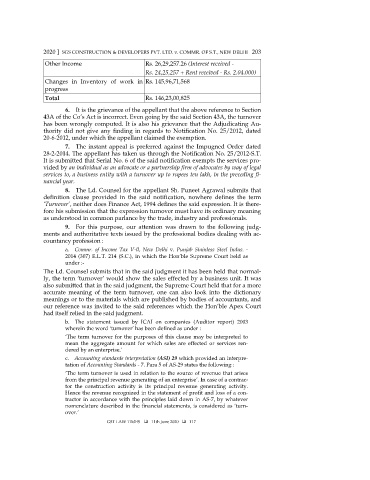

Other Income Rs. 26,29,257.26 (Interest received -

Rs. 24,25,257 + Rent received - Rs. 2.04.000)

Changes in Inventory of work in Rs. 145,96,71,568

progress

Total Rs. 146,23,00,825

6. It is the grievance of the appellant that the above reference to Section

43A of the Co’s Act is incorrect. Even going by the said Section 43A, the turnover

has been wrongly computed. It is also his grievance that the Adjudicating Au-

thority did not give any finding in regards to Notification No. 25/2012, dated

20-6-2012, under which the appellant claimed the exemption.

7. The instant appeal is preferred against the Impugned Order dated

28-2-2014. The appellant has taken us through the Notification No. 25/2012-S.T.

It is submitted that Serial No. 6 of the said notification exempts the services pro-

vided by an individual as an advocate or a partnership firm of advocates by way of legal

services to, a business entity with a turnover up to rupees ten lakh, in the preceding fi-

nancial year.

8. The Ld. Counsel for the appellant Sh. Puneet Agrawal submits that

definition clause provided in the said notification, nowhere defines the term

‘Turnover’, neither does Finance Act, 1994 defines the said expression. It is there-

fore his submission that the expression turnover must have its ordinary meaning

as understood in common parlance by the trade, industry and professionals.

9. For this purpose, our attention was drawn to the following judg-

ments and authoritative texts issued by the professional bodies dealing with ac-

countancy profession :

a. Commr. of Income Tax V-ll, New Delhi v. Punjab Stainless Steel Indus. -

2014 (307) E.L.T. 214 (S.C.), in which the Hon’ble Supreme Court held as

under :-

The Ld. Counsel submits that in the said judgment it has been held that normal-

ly, the term ‘turnover’ would show the sales effected by a business unit. It was

also submitted that in the said judgment, the Supreme Court held that for a more

accurate meaning of the term turnover, one can also look into the dictionary

meanings or to the materials which are published by bodies of accountants, and

our reference was invited to the said references which the Hon’ble Apex Court

had itself relied in the said judgment.

b. The statement issued by ICAI on companies (Auditor report) 2003

wherein the word ‘turnover’ has been defined as under :

‘The term turnover for the purposes of this clause may be interpreted to

mean the aggregate amount for which sales are effected or services ren-

dered by an enterprise.’

c. Accounting standards interpretation (ASI) 29 which provided an interpre-

tation of Accounting Standards - 7. Para 5 of AS-29 states the following :

‘The term turnover is used in relation to the source of revenue that arises

from the principal revenue generating of an enterprise’. In case of a contrac-

tor the construction activity is its principal revenue generating activity.

Hence the revenue recognized in the statement of profit and loss of a con-

tractor in accordance with the principles laid down in AS-7, by whatever

nomenclature described in the financial statements, is considered as ‘turn-

over.’

GST LAW TIMES 11th June 2020 117