Page 30 - GSTL_11th June 2020_Vol 37_Part 2

P. 30

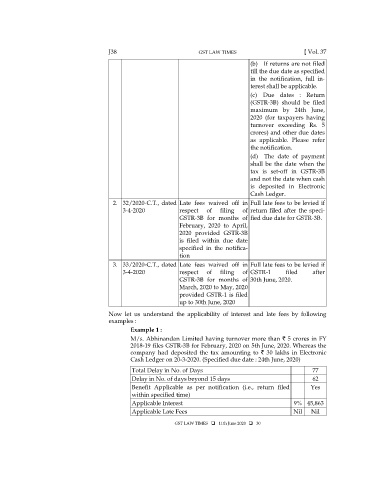

J38 GST LAW TIMES [ Vol. 37

(b) If returns are not filed

till the due date as specified

in the notification, full in-

terest shall be applicable.

(c) Due dates : Return

(GSTR-3B) should be filed

maximum by 24th June,

2020 (for taxpayers having

turnover exceeding Rs. 5

crores) and other due dates

as applicable. Please refer

the notification.

(d) The date of payment

shall be the date when the

tax is set-off in GSTR-3B

and not the date when cash

is deposited in Electronic

Cash Ledger.

2. 32/2020-C.T., dated Late fees waived off in Full late fees to be levied if

3-4-2020 respect of filing of return filed after the speci-

GSTR-3B for months of fied due date for GSTR-3B.

February, 2020 to April,

2020 provided GSTR-3B

is filed within due date

specified in the notifica-

tion

3. 33/2020-C.T., dated Late fees waived off in Full late fees to be levied if

3-4-2020 respect of filing of GSTR-1 filed after

GSTR-3B for months of 30th June, 2020.

March, 2020 to May, 2020

provided GSTR-1 is filed

up to 30th June, 2020

Now let us understand the applicability of interest and late fees by following

examples :

Example 1 :

M/s. Abhinandan Limited having turnover more than ` 5 crores in FY

2018-19 files GSTR-3B for February, 2020 on 5th June, 2020. Whereas the

company had deposited the tax amounting to ` 30 lakhs in Electronic

Cash Ledger on 20-3-2020. (Specified due date : 24th June, 2020)

Total Delay in No. of Days 77

Delay in No. of days beyond 15 days 62

Benefit Applicable as per notification (i.e., return filed Yes

within specified time)

Applicable Interest 9% 45,863

Applicable Late Fees Nil Nil

GST LAW TIMES 11th June 2020 30