Page 39 - GSTL_11th June 2020_Vol 37_Part 2

P. 39

2020 ] RECOVERY OF ARREARS UNDER GST — A COMPLETE ANALYSIS J47

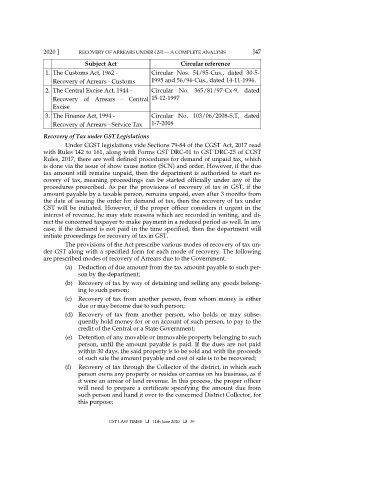

Subject Act Circular reference

1. The Customs Act, 1962 - Circular Nos. 54/95-Cus., dated 30-5-

Recovery of Arrears - Customs 1995 and 56/96-Cus., dated 14-11-1996.

2. The Central Excise Act, 1944 - Circular No. 365/81/97-Cx-9, dated

Recovery of Arrears - Central 15-12-1997

Excise

3. The Finance Act, 1994 - Circular No. 103/06/2008-S.T, dated

Recovery of Arrears - Service Tax 1-7-2008

Recovery of Tax under GST Legislations

Under CGST legislations vide Sections 79-84 of the CGST Act, 2017 read

with Rules 142 to 161, along with Forms GST DRC-01 to GST DRC-25 of CGST

Rules, 2017, there are well defined procedures for demand of unpaid tax, which

is done via the issue of show cause notice (SCN) and order. However, if the due

tax amount still remains unpaid, then the department is authorised to start re-

covery of tax, meaning proceedings can be started officially under any of the

procedures prescribed. As per the provisions of recovery of tax in GST, if the

amount payable by a taxable person, remains unpaid, even after 3 months from

the date of issuing the order for demand of tax, then the recovery of tax under

GST will be initiated. However, if the proper officer considers it urgent in the

interest of revenue, he may state reasons which are recorded in writing, and di-

rect the concerned taxpayer to make payment in a reduced period as well. In any

case, if the demand is not paid in the time specified, then the department will

initiate proceedings for recovery of tax in GST.

The provisions of the Act prescribe various modes of recovery of tax un-

der GST along with a specified form for each mode of recovery. The following

are prescribed modes of recovery of Arrears due to the Government.

(a) Deduction of due amount from the tax amount payable to such per-

son by the department;

(b) Recovery of tax by way of detaining and selling any goods belong-

ing to such person;

(c) Recovery of tax from another person, from whom money is either

due or may become due to such person;

(d) Recovery of tax from another person, who holds or may subse-

quently hold money for or on account of such person, to pay to the

credit of the Central or a State Government;

(e) Detention of any movable or immovable property belonging to such

person, until the amount payable is paid. If the dues are not paid

within 30 days, the said property is to be sold and with the proceeds

of such sale the amount payable and cost of sale is to be recovered;

(f) Recovery of tax through the Collector of the district, in which such

person owns any property or resides or carries on his business, as if

it were an arrear of land revenue. In this process, the proper officer

will need to prepare a certificate specifying the amount due from

such person and hand it over to the concerned District Collector, for

this purpose;

GST LAW TIMES 11th June 2020 39