Page 109 - GSTL_18th June 2020_Vol 37_Part 3

P. 109

2020 ] SURYA ENTERPRISES v. COMMISSIONER OF C. EX. & S.T., CHENNAI-III 323

(iii) requiring production of accounts, documents or other evi-

dence under the Chapter or the rules made thereunder; or

(b) an audit has been initiated, and such inquiry, investigation or audit

is pending as on the 1st day of March, 2013, then, the designated au-

thority shall, by an order, and for reasons to be recorded in writing,

reject such declaration.

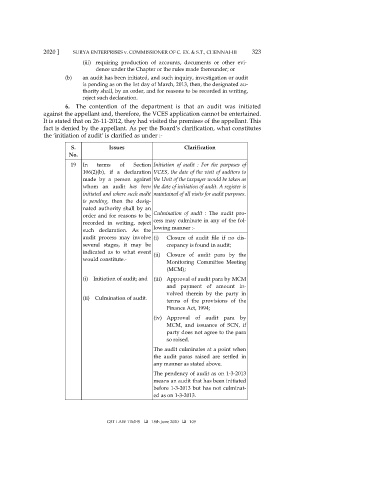

6. The contention of the department is that an audit was initiated

against the appellant and, therefore, the VCES application cannot be entertained.

It is stated that on 26-11-2012, they had visited the premises of the appellant. This

fact is denied by the appellant. As per the Board’s clarification, what constitutes

the ‘initiation of audit’ is clarified as under :-

S. Issues Clarification

No.

19 In terms of Section Initiation of audit : For the purposes of

106(2)(b), if a declaration VCES, the date of the visit of auditors to

made by a person against the Unit of the taxpayer would be taken as

whom an audit has been the date of initiation of audit. A register is

initiated and where such audit maintained of all visits for audit purposes.

is pending, then the desig-

nated authority shall by an

order and for reasons to be Culmination of audit : The audit pro-

recorded in writing, reject cess may culminate in any of the fol-

such declaration. As the lowing manner :-

audit process may involve (i) Closure of audit file if no dis-

several stages, it may be crepancy is found in audit;

indicated as to what event (ii) Closure of audit para by the

would constitute.- Monitoring Committee Meeting

(MCM);

(i) Initiation of audit; and (iii) Approval of audit para by MCM

and payment of amount in-

volved therein by the party in

(ii) Culmination of audit. terms of the provisions of the

Finance Act, 1994;

(iv) Approval of audit para by

MCM, and issuance of SCN, if

party does not agree to the para

so raised.

The audit culminates at a point when

the audit paras raised are settled in

any manner as stated above.

The pendency of audit as on 1-3-2013

means an audit that has been initiated

before 1-3-2013 but has not culminat-

ed as on 1-3-2013.

GST LAW TIMES 18th June 2020 109