Page 65 - GSTL_18th June 2020_Vol 37_Part 3

P. 65

2020 ] SUPRASESH GENERAL INSURANCE SERVICE & BROKERS v. ASSTT. COMMR. 279

under VCES was in compliance with the said rules. Therefore, the proposal to

invoke the Second Proviso to Section 106(1) of the Act is also unjustified.

8. In support of the present writ petition, the Learned Counsel for the

petitioner drew my attention to the decision of the different High Courts dealing

with almost the identical situation relating to aforesaid scheme eligibility on

amounts paid prior to passing of the Finance Act, 2013 in Sadguru Construction

Co. v. Union of India, (2015) 81 VST 95 (Guj.) = 2014 (36) S.T.R. 3 (Guj.) and in Su-

prasesh General Insurance Services and Brokers (P) Ltd. v. Commissioner of Service Tax,

(2015) 86 VST 160 (Mad) = 2016 (41) S.T.R. 34 (Mad.) and in Premier Associates v.

Assistant Commissioner of Service Tax, (2018) 49 GSTR 1 (Karn).

9. The Learned Counsel also drew attention to the decision of the Kera-

la High Court in Alwaye Sugar Agency v. Commercial Tax Officer, Alwaye and Oth-

ers, (2011) 42 VST 517 (Ker), wherein, the Court considered an identical situation

and held that if benefit is not given, it would lead to a very anomalous situation.

10. The Learned Counsel for the respondent submits that the impugned

order cannot be challenged in this writ petition as the petitioner has an alternate

remedy by way of appeal under Section 84 of the Finance Act, 1997 and there-

fore, the writ petition was liable to be dismissed.

11. The Learned Counsel for the respondent further submitted that the

issue as to whether payments made prior to enactment of Finance Act, 2013, can

be considered for settling dispute under the aforesaid scheme, is clearly covered

against the petitioner by the decision of the Calcutta High Court in Durgapur Die-

sel Sales and Service v. Superintendent (Service Tax) Central Excise, Durgapur, (2015)

59 taxmann.com 407 (Calcutta) = 2015 (38) S.T.R. 1129 (Cal.), wherein, the deci-

sion of the Delhi High Court [2014 (34) S.T.R. 165 (Del.)] has been distinguished.

The Learned Counsel for the respondent also submitted that the payment were

made prior to the enactment of the Finance Act, 2013, the aforesaid payment

cannot be considered for the purpose of the Service Tax Voluntary Compliance

Encouragement Scheme, 2013 in the light of the clarification of Central Board

Excise and Customs (CBEC) in Circular No. 170/58/2013-S.T., dated 8-8-2013.

12. I have heard the Learned Counsel for the petitioner and the

Learned Standing Counsel for the respondent. I have also perused the provisions

of the Finance Act, 2013, in terms of which the Service Tax Voluntary Compli-

ance Encouragement Scheme, 2013 was announced.

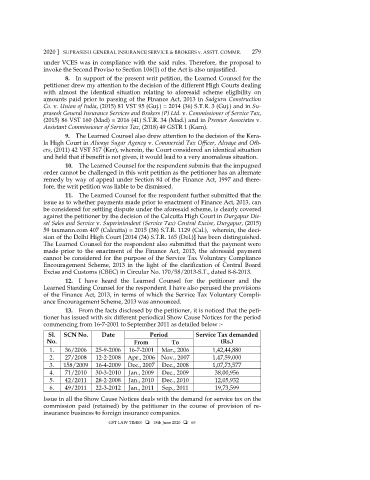

13. From the facts disclosed by the petitioner, it is noticed that the peti-

tioner has issued with six different periodical Show Cause Notices for the period

commencing from 16-7-2001 to September 2011 as detailed below :-

Sl. SCN No. Date Period Service Tax demanded

No. From To (Rs.)

1. 36/2006 25-9-2006 16-7-2001 Mar., 2006 1,42,44,880

2. 27/2008 12-2-2008 Apr., 2006 Nov., 2007 1,47,59,000

3. 158/2009 16-4-2009 Dec., 2007 Dec., 2008 1,07,73,577

4. 71/2010 30-3-2010 Jan., 2009 Dec., 2009 38,00,956

5. 42/2011 28-2-2008 Jan., 2010 Dec., 2010 12,05,932

6. 49/2011 22-3-2012 Jan., 2011 Sep., 2011 19,73,599

Issue in all the Show Cause Notices deals with the demand for service tax on the

commission paid (retained) by the petitioner in the course of provision of re-

insurance business to foreign insurance companies.

GST LAW TIMES 18th June 2020 65