Page 67 - GSTL_18th June 2020_Vol 37_Part 3

P. 67

2020 ] SUPRASESH GENERAL INSURANCE SERVICE & BROKERS v. ASSTT. COMMR. 281

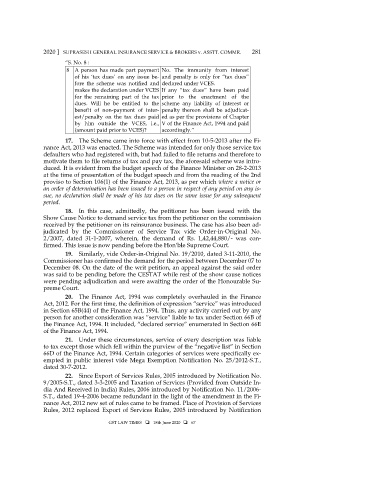

“S. No. 8 :

8 A person has made part payment No. The immunity from interest

of his ‘tax dues’ on any issue be- and penalty is only for “tax dues”

fore the scheme was notified and declared under VCES.

makes the declaration under VCES If any “tax dues” have been paid

for the remaining part of the tax prior to the enactment of the

dues. Will he be entitled to the scheme any liability of interest or

benefit of non-payment of inter- penalty thereon shall be adjudicat-

est/penalty on the tax dues paid ed as per the provisions of Chapter

by him outside the VCES, i.e., V of the Finance Act, 1994 and paid

(amount paid prior to VCES)? accordingly.”

17. The Scheme came into force with effect from 10-5-2013 after the Fi-

nance Act, 2013 was enacted. The Scheme was intended for only those service tax

defaulters who had registered with, but had failed to file returns and therefore to

motivate them to file returns of tax and pay tax, the aforesaid scheme was intro-

duced. It is evident from the budget speech of the Finance Minister on 28-2-2013

at the time of presentation of the budget speech and from the reading of the 2nd

proviso to Section 106(1) of the Finance Act, 2013, as per which where a notice or

an order of determination has been issued to a person in respect of any period on any is-

sue, no declaration shall be made of his tax dues on the same issue for any subsequent

period.

18. In this case, admittedly, the petitioner has been issued with the

Show Cause Notice to demand service tax from the petitioner on the commission

received by the petitioner on its reinsurance business. The case has also been ad-

judicated by the Commissioner of Service Tax vide Order-in-Original No.

2/2007, dated 31-1-2007, wherein, the demand of Rs. 1,42,44,880/- was con-

firmed. This issue is now pending before the Hon’ble Supreme Court.

19. Similarly, vide Order-in-Original No. 19/2010, dated 3-11-2010, the

Commissioner has confirmed the demand for the period between December 07 to

December 08. On the date of the writ petition, an appeal against the said order

was said to be pending before the CESTAT while rest of the show cause notices

were pending adjudication and were awaiting the order of the Honourable Su-

preme Court.

20. The Finance Act, 1994 was completely overhauled in the Finance

Act, 2012. For the first time, the definition of expression “service” was introduced

in Section 65B(44) of the Finance Act, 1994. Thus, any activity carried out by any

person for another consideration was “service” liable to tax under Section 66B of

the Finance Act, 1994. It included, “declared service” enumerated in Section 66E

of the Finance Act, 1994.

21. Under these circumstances, service of every description was liable

to tax except those which fell within the purview of the “negative list” in Section

66D of the Finance Act, 1994. Certain categories of services were specifically ex-

empted in public interest vide Mega Exemption Notification No. 25/2012-S.T.,

dated 30-7-2012.

22. Since Export of Services Rules, 2005 introduced by Notification No.

9/2005-S.T., dated 3-3-2005 and Taxation of Services (Provided from Outside In-

dia And Received in India) Rules, 2006 introduced by Notification No. 11/2006-

S.T., dated 19-4-2006 became redundant in the light of the amendment in the Fi-

nance Act, 2012 new set of rules came to be framed. Place of Provision of Services

Rules, 2012 replaced Export of Services Rules, 2005 introduced by Notification

GST LAW TIMES 18th June 2020 67