Page 195 - GSTL_2nd July 2020 _Vol 38_Part 1

P. 195

2020 ] IN RE : SUPERNOVA ENGINEERS LTD. 113

2020 (38) G.S.T.L. 113 (Commr. Appl. - GST - Guj.)

BEFORE THE COMMISSIONER OF GST (APPEALS), AHMEDABAD

Shri Uma Shanker, Commissioner (Appeals)

IN RE : SUPERNOVA ENGINEERS LTD.

Order-in-Appeal No. AHM-EXCUS-003-APP-146 to 153-18-19, dated 27-12-2018

Refund of unutilized credit - Multiple inputs attracting different rates

of tax - “Net ITC “ as per formula given in Rule 89(5) of Central Goods and

Services Tax Rules, 2017 covers the ITC availed on all inputs in the relevant

period, irrespective of their rate of tax - Net ITC as per definition mentioned in

Rule 89(5) ibid to be followed - Calculation of net ITC after deduction of in-

verted rate purchase ITC, i.e., lower rated purchase not correct - Refund admis-

sible - Section 54 of Central Goods and Services Tax Act, 2017. [para 6]

Appeals allowed

CASES CITED

Commissioner v. Favourite Industries — 2012 (278) E.L.T. 145 (S.C.) — Relied on ......................... [Para 6]

Duport Steel v. Sirs — 1980 — Relied on ................................................................................................. [Para 6]

State v. Parmeshwaran Subramani — 2009 (242) E.L.T. 162 (S.C.) — Relied on ............................... [Para 6]

Union of India v. Dharamendra Textile Processors — 2008 (231) E.L.T. 3 (S.C.) — Relied on ....... [Para 6]

[Order]. - This order arises on account of appeals filed by M/s. Superno-

va Engineers Ltd., Survey Number 1470/1, Village Rajpur, Taluka - Kadi, Dst.

Mehsana (hereinafter referred to as the ‘the appellants’ for sake of brevity) against

the following two Orders-in-Original (hereinafter referred to as the ‘impugned

orders’ for the sake of brevity) passed by the Assistant Commissioner, CGST, Ka-

di Division, Gandhinagar (hereinafter referred to as the ‘adjudicating authority’ for

the sake of brevity);

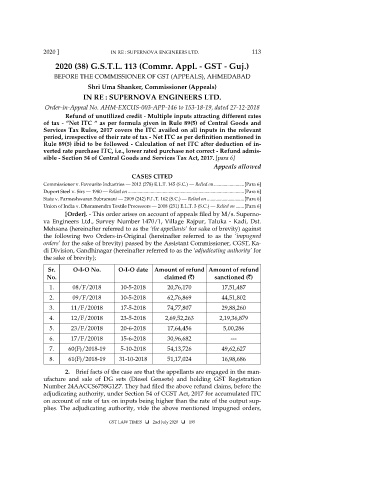

Sr. O-I-O No. O-I-O date Amount of refund Amount of refund

No. claimed (`) sanctioned (`)

1. 08/F/2018 10-5-2018 20,76,170 17,51,487

2. 09/F/2018 10-5-2018 62,76,869 44,51,802

3. 11/F/20018 17-5-2018 74,77,807 29,88,260

4. 12/F/20018 23-5-2018 2,69,52,263 2,19,36,879

5. 23/F/20018 20-6-2018 17,64,456 5,00,286

6. 17/F/20018 15-6-2018 30,96,682 ---

7. 60(F)/2018-19 5-10-2018 54,13,726 49,62,627

8. 61(F)/2018-19 31-10-2018 51,17,024 16,98,686

2. Brief facts of the case are that the appellants are engaged in the man-

ufacture and sale of DG sets (Diesel Gensets) and holding GST Registration

Number 24AACCS6758G1Z7. They had filed the above refund claims, before the

adjudicating authority, under Section 54 of CGST Act, 2017 for accumulated ITC

on account of rate of tax on inputs being higher than the rate of the output sup-

plies. The adjudicating authority, vide the above mentioned impugned orders,

GST LAW TIMES 2nd July 2020 195