Page 131 - GSTL_16th July 2020_Vol. 38_Part 3

P. 131

2020 ] IN RE : JVS FOODS PVT. LTD. 369

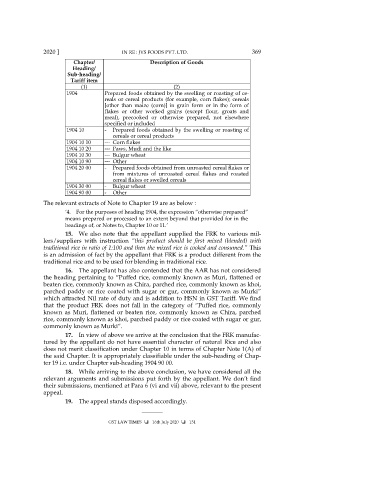

Chapter/ Description of Goods

Heading/

Sub-heading/

Tariff item

(1) (2)

1904 Prepared foods obtained by the swelling or roasting of ce-

reals or cereal products (for example, corn flakes); cereals

[other than maize (corn)] in grain form or in the form of

flakes or other worked grains (except flour, groats and

meal), precooked or otherwise prepared, not elsewhere

specified or included

1904 10 - Prepared foods obtained by the swelling or roasting of

cereals or cereal products

1904 10 10 --- Corn flakes

1904 10 20 --- Paws, Mudi and the like

1904 10 30 --- Bulgur wheat

1904 10 90 --- Other

1904 20 00 - Prepared foods obtained from unroasted cereal flakes or

from mixtures of unroasted cereal flakes and roasted

cereal flakes or swelled cereals

1904 30 00 - Bulgur wheat

1904 90 00 - Other

The relevant extracts of Note to Chapter 19 are as below :

‘4. For the purposes of heading 1904, the expression “otherwise prepared”

means prepared or processed to an extent beyond that provided for in the

headings of, or Notes to, Chapter 10 or 11.’

15. We also note that the appellant supplied the FRK to various mil-

lers/suppliers with instruction “this product should be first mixed (blended) with

traditional rice in ratio of 1:100 and then the mixed rice is cooked and consumed.” This

is an admission of fact by the appellant that FRK is a product different from the

traditional rice and to be used for blending in traditional rice.

16. The appellant has also contended that the AAR has not considered

the heading pertaining to “Puffed rice, commonly known as Muri, flattened or

beaten rice, commonly known as Chira, parched rice, commonly known as khoi,

parched paddy or rice coated with sugar or gur, commonly known as Murki”

which attracted Nil rate of duty and is addition to HSN in GST Tariff. We find

that the product FRK does not fall in the category of “Puffed rice, commonly

known as Muri, flattened or beaten rice, commonly known as Chira, parched

rice, commonly known as khoi, parched paddy or rice coated with sugar or gur,

commonly known as Murki”.

17. In view of above we arrive at the conclusion that the FRK manufac-

tured by the appellant do not have essential character of natural Rice and also

does not merit classification under Chapter 10 in terms of Chapter Note 1(A) of

the said Chapter. It is appropriately classifiable under the sub-heading of Chap-

ter 19 i.e. under Chapter sub-heading 1904 90 00.

18. While arriving to the above conclusion, we have considered all the

relevant arguments and submissions put forth by the appellant. We don’t find

their submissions, mentioned at Para 6 (vi and vii) above, relevant to the present

appeal.

19. The appeal stands disposed accordingly.

_______

GST LAW TIMES 16th July 2020 131