Page 178 - GSTL_16th July 2020_Vol. 38_Part 3

P. 178

416 GST LAW TIMES [ Vol. 38

but our money consideration for the same is through raising of un-

distributed bills on output per ton basis;

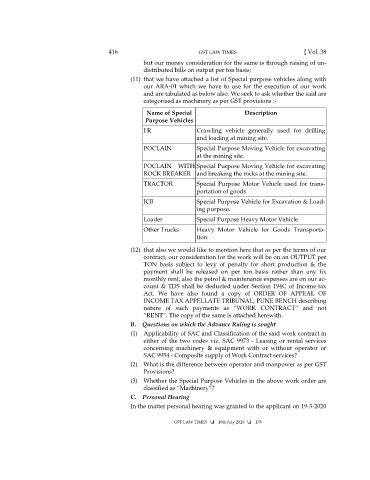

(11) that we have attached a list of Special purpose vehicles along with

our ARA-01 which we have to use for the execution of our work

and are tabulated as below also. We seek to ask whether the said are

categorised as machinery as per GST provisions :-

Name of Special Description

Purpose Vehicles

I R Crawling vehicle generally used for drilling

and loading at mining site.

POCLAIN Special Purpose Moving Vehicle for excavating

at the mining site.

POCLAIN WITH Special Purpose Moving Vehicle for excavating

ROCK BREAKER and breaking the rocks at the mining site.

TRACTOR Special Purpose Motor Vehicle used for trans-

portation of goods

JCB Special Purpose Vehicle for Excavation & Load-

ing purpose.

Loader Special Purpose Heavy Motor Vehicle

Other Trucks Heavy Motor Vehicle for Goods Transporta-

tion.

(12) that also we would like to mention here that as per the terms of our

contract, our consideration for the work will be on an OUTPUT per

TON basis subject to levy of penalty for short production & the

payment shall be released on per ton basis rather than any fix

monthly rent, also the petrol & maintenance expenses are on our ac-

count & TDS shall be deducted under Section 194C of Income-tax

Act. We have also found a copy of ORDER OF APPEAL OF

INCOME TAX APPELLATE TRIBUNAL, PUNE BENCH describing

nature of such payments as “WORK CONTRACT” and not

“RENT”. The copy of the same is attached herewith.

B. Questions on which the Advance Ruling is sought

(1) Applicability of SAC and Classification of the said work contract in

either of the two codes viz. SAC 9973 - Leasing or rental services

concerning machinery & equipment with or without operator or

SAC 9954 - Composite supply of Work Contract services?

(2) What is the difference between operator and manpower as per GST

Provisions?

(3) Whether the Special Purpose Vehicles in the above work order are

classified as “Machinery”?

C. Personal Hearing

In the matter personal hearing was granted to the applicant on 19-3-2020

GST LAW TIMES 16th July 2020 178