Page 188 - GSTL_16th July 2020_Vol. 38_Part 3

P. 188

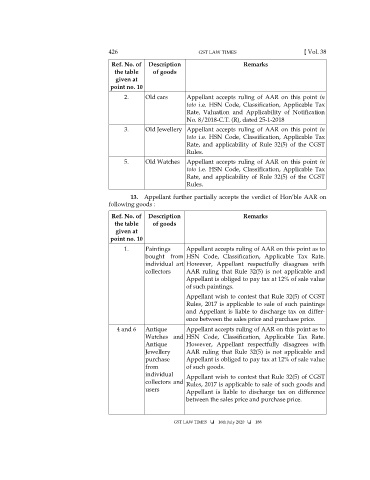

426 GST LAW TIMES [ Vol. 38

Ref. No. of Description Remarks

the table of goods

given at

point no. 10

2. Old cars Appellant accepts ruling of AAR on this point in

toto i.e. HSN Code, Classification, Applicable Tax

Rate, Valuation and Applicability of Notification

No. 8/2018-C.T. (R), dated 25-1-2018

3. Old Jewellery Appellant accepts ruling of AAR on this point in

toto i.e. HSN Code, Classification, Applicable Tax

Rate, and applicability of Rule 32(5) of the CGST

Rules.

5. Old Watches Appellant accepts ruling of AAR on this point in

toto i.e. HSN Code, Classification, Applicable Tax

Rate, and applicability of Rule 32(5) of the CGST

Rules.

13. Appellant further partially accepts the verdict of Hon’ble AAR on

following goods :

Ref. No. of Description Remarks

the table of goods

given at

point no. 10

1. Paintings Appellant accepts ruling of AAR on this point as to

bought from HSN Code, Classification, Applicable Tax Rate.

individual art However, Appellant respectfully disagrees with

collectors AAR ruling that Rule 32(5) is not applicable and

Appellant is obliged to pay tax at 12% of sale value

of such paintings.

Appellant wish to contest that Rule 32(5) of CGST

Rules, 2017 is applicable to sale of such paintings

and Appellant is liable to discharge tax on differ-

ence between the sales price and purchase price.

4 and 6 Antique Appellant accepts ruling of AAR on this point as to

Watches and HSN Code, Classification, Applicable Tax Rate.

Antique However, Appellant respectfully disagrees with

Jewellery AAR ruling that Rule 32(5) is not applicable and

purchase Appellant is obliged to pay tax at 12% of sale value

from of such goods.

individual Appellant wish to contest that Rule 32(5) of CGST

collectors and Rules, 2017 is applicable to sale of such goods and

users Appellant is liable to discharge tax on difference

between the sales price and purchase price.

GST LAW TIMES 16th July 2020 188